How Neoliberalism Has Wielded ‘Corruption’ to Privatise Life in Africa

In Africa, the leading forces of capitalism have ruthlessly wielded a neoliberal conception of corruption to undermine states’ sovereignty and open the continent to plunder at the hands of Western multinational corporations.

The dossier was researched and written under the leadership of Professor Grieve Chelwa of The Africa Institute, Global Studies University, through Tricontinental Pan Africa.

The artwork in this dossier attempts to illustrate the true face of corruption on the African continent – from the brutal plunder of the colonial era to today’s legalised looting by multinational corporations through tax evasion and other illicit forms of accounting. The satirical images aim to subvert the racialised image of African corruption and highlight the true cost of neo-colonialism and the faces of the true culprits – the Western multinational corporations, banks, and accounting institutions who underdevelop Africa for their own profit.

In the years following the fall of the Soviet Union, the word ‘corruption’ increasingly began to appear in the reports of multilateral agencies and non-governmental organisations. These reports argued that corruption is rooted in the regulatory function of states, which control large-scale development projects and whose officials oversee the delivery of licences and permits; if the regulatory function of states could be minimised, many of these reports argued, corruption would be less pervasive. This kind of anti-corruption discourse fit neatly within the neoliberal drive to shrink states’ regulatory apparatuses, deregulate and privatise economic activity, and promote the idea that the freedom of the market’s invisible hand would create a moral foundation for society.

Yet, none of these reports – including those from the World Bank and Transparency International – offered a clear definition of corruption. In The Anti-Corruption Plain Language Guide (2009), Transparency International defined corruption as ‘the abuse of entrusted power for private gain’.1 Three years later, the World Bank described corruption as ‘the abuse of public office for private gain’.2 These definitions are similar, and they continue to be reproduced in reports from multilateral organisations and in academic scholarship. The key word here is ‘abuse’, and the main implication is that someone in the public sector entrusted with power or public office abuses their role for private gain, such as through bribery, nepotism, extortion, and embezzlement. This orientation argues that if the state were smaller or more disciplined, there would be little to no corruption in society. Even though the non-governmental organisation Transparency International added a concern about private sector corruption in 2010, this addition has been marginal to the overall focus on public sector corruption.3

The epicentre of this argument has been the African continent, where the idea of ‘corruption’ – meaning corruption of the state – has effectively been used to diminish the state’s regulatory functions and reduce the number of state employees. It is important to note that while 21% of the European workforce, on average, is employed in the public sector, that number is a mere 2.38% in Mali, 3.6% in Nigeria, and 6.7% in Zambia, which in turn limits these states’ capacity to manage and regulate large multinational corporations on the African continent.4 Furthermore, over the course of the 1990s and the 2000s, the International Monetary Fund (IMF) fought to reduce public-sector employees’ salaries, which certainly increases the likelihood of bribery. The IMF outlined this approach in its 1991 Public Expenditure Handbook, which makes reducing the wage bill for public-sector workers a central part of its agenda.5

In neoliberal literature, corruption primarily takes the form of bribery, extortion, and embezzlement – all of which refer principally to public sector corruption – while omitting concepts such as transfer mispricing, trade mis-invoicing, accounting irregularities, financial mismanagement, and tax avoidance – all of which are essential elements of multinational corporations’ accounting practices.6 There are a range of socio-psychological reasons for corruption, the most referenced one being greed. But greed is not a transhistorical concept or emotion; rather, it is shaped by the social formation in which it is allowed to grow. Capitalism has a special relationship to greed, since it fosters the ‘animal spirits’ (as the economist John Maynard Keynes put it) to reduce all human life to commodities and to centralise the profit motive as the economic motor.7 Yet, older forms of morality that are eager to set aside hypocrisy and overcome the dominion of money prevail in social consciousness across the world. This dossier is anchored in the popular sentiment against corruption in society, driven largely not by petty bribery but by industrial-scale corruption by private capital. The Malaysian sociologist Syed Hussein Alatas called this ‘tidal corruption’: the corruption that ‘floods the entire state apparatus involving those at the centre of power. Like the tide, it rises to cover wider areas and immerse the surrounding vegetation’.8 This dossier is not a defence of corruption; on the contrary, it argues for an understanding of corruption that is not rooted solely in the public sector but that appreciates the tidal corruption set in motion by the leading forces of capitalism. It focuses on the African continent because that is where agencies such as the IMF and the World Bank have most effectively wielded the idea of ‘corruption’ to undermine states’ sovereignty and subjugate the countries of the Global South to the extraordinary power of multinational corporations, particularly in the mining sector.9

Part 1: The Neoliberal Corruption Industry

In 1993, Peter Eigen, a German lawyer who worked at the World Bank in the legal department, registered an association in Germany called Transparency International. Eigen worked with Michael Wiehen (formerly of the World Bank) and Hansjörg Elshorst (formerly of the German Agency for Technical Cooperation) to establish Transparency International in German business and government circles as a legitimate organisation. Before going forward to discipline countries of the Global South, the association had to ensure that European states had built their own legitimacy regarding corruption. That is why they lobbied the governments of France and Germany to stop the policy of what, in Germany, is called Schmiergeld (bribe money); these countries not only allowed bribes to be paid in foreign jurisdictions, but then permitted companies to deduct these payments from tax obligations.10 This lobbying resulted in the passage of the 1999 Organisation for Economic Cooperation and Development (OECD) Convention on Combating the Bribery of Foreign Public Officials in International Business Transactions. By passing this convention, European officials and their counterparts in North America created a framework about corruption through which to adopt a morally superior position over governments in the Global South.11 In 1997, Matthew Parris, a conservative South African-born member of the British Parliament, said, ‘Corruption has become an African epidemic. It is impossible to overstate the poisoning of human relations and the paralysing of initiative that corruption on the African scale brings’.12 This phrase – on the African scale – defines an attitude toward corruption that embodies both the long colonial history of theft and the neocolonial present of corporate malfeasance on the continent.

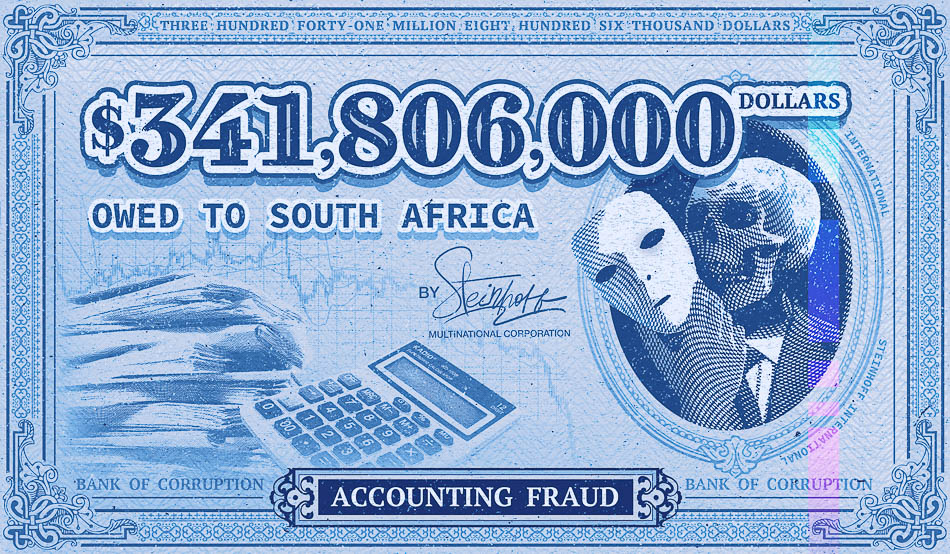

Yet those who moralise about African corruption have little to say when it comes to the criminality of corporate corruption. Take, for example, the German-South African retail giant Steinhoff International (1964–2023). In 2015, German officials raided the offices of Steinhoff Europe Group Services as part of an investigation into accounting fraud. As the scandal became too big to contain, with new investigations by contracted firms such as PricewaterhouseCoopers, and with Steinhoff’s senior management forced to resign, the South African parliament opened its own investigation of the firm, which found that businesses such as Steinhoff rely upon public funds for their investments, including – in the case of South Africa – the Public Investment Corporation.13 These public funds lost billions in Steinhoff’s eventual collapse. In 2019, South Africa’s Financial Sector Conduct Authority imposed an administrative fine of ZAR 1.5 billion (US $95 million) on the company for false, misleading, or deceptive statements to the market. This fine was later reduced to ZAR 53 million (US $3.4 million), a minuscule amount compared to the approximately ZAR 124.9 billion (US $6.9 billion) involved in fictitious or irregular transactions that substantially inflated Steinhoff’s profits and assets between 2009 and 2017.14 In the service of ‘investor-friendly policies’, these scandals are either underreported or treated as the exception rather than the rule. Yet this is a familiar story, from the accounting debacles at Enron Corporation (2001) and Arthur Andersen (2002) – which led to the largest known case of corporate fraud in history – to the faked emissions scandal at Volkswagen (2015).

Before Transparency

In the period of decolonisation and then of the formation of post-colonial states, Western-driven modernisation theory argued that corruption was not a ‘poison’ but an asset that helped shape the relationship between the ruling class and the state apparatus. Drawing from the experience of the United States, Robert K. Merton’s Social Theory and Social Structure (1949) provided the basis for this line of argument: that corruption made the relationship between state officials and the ruling class more intimate.15 In the 1960s, a range of influential scholars published important articles based on fieldwork in Africa and Asia to substantiate the claim that corruption ‘humanises government’, as Edward Shils wrote in 1960.16 Indeed, in his classic work Political Order in Changing Societies (1968), Samuel Huntington argued that corruption (or what he defined as ‘patronage from above’) in Africa, Asia, and Latin America had contributed to the creation of ‘the most effective political parties and most stable political systems’.17 In this Western modernisation literature, which dominated the worldview of multilateral institutions, corruption was treated as an utterly normal – even beneficial – form of economic interaction.

Modernisation theory played a considerable role in the new post-colonial states, but it was not the only approach to economic development. In 1955, the Bandung Final Communiqué made it clear that the most predatory aspect of the world economy’s neocolonial structure was the role of transnational corporations (TNCs), as they were known then (later called multinational corporations, or MNCs). Many of these TNCs, which emerged during the colonial era, had built up their capital stock through colonial theft and structured world economic relations to gain privileged access to raw materials in the former colonies as well as captive markets to which to export their expensive finished products. That is why the new post-colonial states centred the role of TNCs as they developed the platform of the New International Economic Order (NIEO): if these states were to establish sovereignty over their own territories, they had to reduce the power of TNCs either by regulation or restriction.18 Since many of these states lacked the capacity to develop an in-depth analysis of how these firms were organised or how they managed their financial transactions, they urged the UN Conference on Trade and Development (UNCTAD) and other United Nations bodies to do so. In 1974, the UN Centre for Transnational Corporations (UNCTC) was created for this purpose and began to build a database on the major TNCs’ operations in order to understand what was seen as the institutionalisation of corruption through novel manoeuvres of accounting.

At the same time, the post-colonial states understood the grave limitations they had inherited from their old colonial masters all too well, such as a hierarchical state apparatus designed to terrorise the colonised population and a bureaucracy that had been trained to serve the ends of colonialism, not the people. With the departure of the colonial bureaucrats, the now independent states had to train almost an entirely new administration, many of whose cadre came from impoverished or near-impoverished backgrounds (material conditions that increased the temptation to accept bribes). These states opened public administration institutes to develop the capacity of their new employees and to encourage them to work with the spirit of the national liberation struggles that had won them independence. Each state’s attitude towards public administration varied based on its class politics: in states with a more landlord-bourgeois character, the public administration institutes inherited the old colonial forms of bureaucracy without much revision, whereas states with a higher socialist character (such as China and Vietnam) emphasised combatting the forms of hierarchy amongst state officials. In Vietnam, for instance, Ho Chi Minh called upon the new workers to lead by example rather than corrupt society with bribery and extortion (Thi đua là yêu nước, yêu nước thì phải thi đua, Ho Chi Minh said: ‘emulation is patriotism; patriots must emulate’).19 Since the material conditions to build a new kind of state simply did not exist, modern training and social pressure became the primary avenues through which to inculcate new values against a backdrop of low salaries and great temptations (the ‘creation of a new man’, as Ernesto ‘Che’ Guevara wrote).20 Yet, in the era ‘before transparency’, under pressure from TNCs and from Western modernisation theory which justified bribery, post-colonial governments struggled to produce new state values.

The Age of Transparency

In the 1990s, a new argument emerged from the Western academy and multilateral organisations controlled by Western governments. This new theory, which moved from modernisation to neoliberal theory, suggested that the states in the Global South were the locus of corruption, that a smaller state would largely solve the problem, and that more pressure must be placed on these states in order to ‘discipline’ them. The idea that TNCs – now MNCs (multinational corporations) – could be corrupt completely vanished in this theory.

In 1992, under pressure from the US government, the UNCTC was integrated into UNCTAD, where its mandate was radically transformed. Instead of being a watchdog of these large corporations, the UNCTC put its resources toward helping MNCs enter southern markets. There was no more interest in producing a TNC Code of Conduct, the skeleton of which was relegated to a languishing draft from 1983 that is raised every few years and thereafter ignored in special sessions.21 In other words, the UNCTC became largely moot. What is truly remarkable is that the UNCTC and its code of conduct were sidelined by the West just when UNCTAD showed that 80% of global trade (in terms of gross exports) was linked to the international production networks of these mega corporations that operated across national boundaries, and that the market was becoming increasingly concentrated around these firms.22 That is largely why multilateral agencies make no mention of the private sector in their definition of corruption, which they describe as merely the ‘abuse of public office for private gain’.

In 1995, in place of the UNCTC’s TNC Code of Conduct, Transparency International released its annual Corruption Perceptions Index (CPI).23 The CPI was measured by a group of ‘experts’ (often private businessmen) who offered their subjective assessment of public sector corruption in various countries. Even when the CPI redefined corruption in 2010 as ‘the abuse of entrusted power for private gain, encompassing practices in both the public and private sectors’, it still ranked countries based on the perception of corruption in the public sector.24 The underlying neoliberal theory here is that corruption in the public sector corrodes the quality of investments in public goods, as corrupt officials seek to increase the volume of investments in order to increase bribes without considering how those investments align with broader national development goals. According to this theory, the correct course is more privatisation and less government oversight; its proposal for ‘transparency’ is merely to eviscerate regulatory state apparatuses and exaggerate the private sector’s ability to profit from public goods.

Under pressure from Transparency International and allied Western governments, the United Nations General Assembly adopted the UN Convention Against Corruption in 2003, which was replicated in the 2003 African Union Convention on Preventing and Combating Corruption. The UN and African Union (AU) treaties do not explicitly define corruption; rather, they make a list of offences that they suggest should be criminalised, which overwhelmingly focuses on the public sector (such as bribery of public officials).25 The UN convention, AU convention, and Transparency International’s CPI treat various types of theft as perfectly legal, including the legal theft of surplus value from workers, the illegal deductions of fines and fees used to penalise workers, and corruption legalised by accountants. By turning a blind eye to corporate corruption and focusing, instead, on bribes of public officials, these entities normalise the structured criminality of capitalism. Furthermore, the Western-driven UN Convention and the Western-based NGO (Transparency International) that have taken charge of this discourse of corruption have made it appear as though the West has transcended corruption and that corruption is primarily a problem in the Global South. This narrative exculpates the Western-based MNCs from blame and erases the long anti-corruption struggles in the Global South, a rich ethical tradition that is rooted both in religion and in common sense.

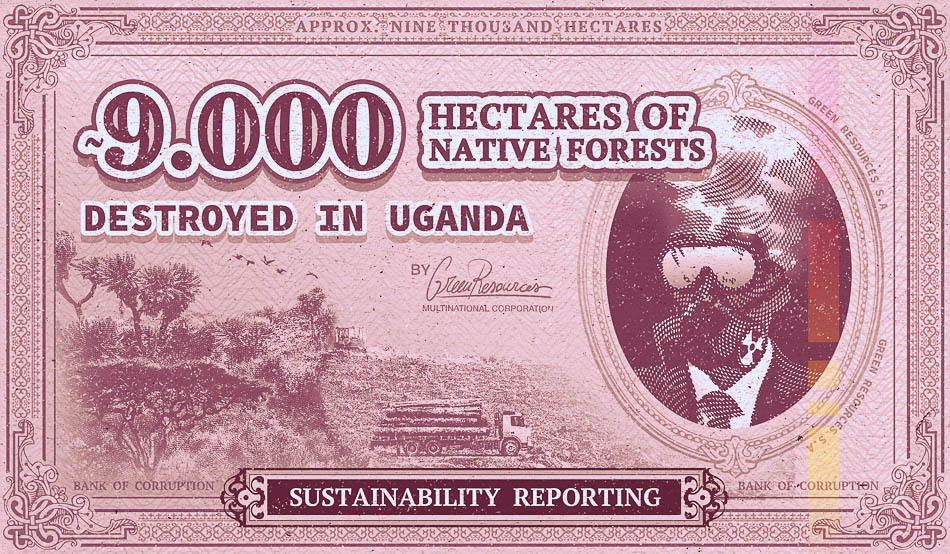

Meanwhile, the world of accounting has developed a new form of theft called ‘sustainability reporting’, which is emblematic of a broader trend that seeks ways to hide money from tax authorities and legalise corruption. This form of greenwashing allows accounting firms to disclose what they are doing to incorporate environmental, social, and governance (ESG) factors in order to discount their taxable income, and in so doing often providing false or misleading claims about the environmental benefits of a product, service, or investment.26 Furthermore, these accounting practices are not obligated to produce or follow a proper environmental assessment, nor are they concerned about the displacement of residents from an area of operation, degradation of ecosystems, misuse of agricultural land, consumption of fossil fuel energy, or harsh exploitation of labour. Despite rampant abuse by MNCs – the plastic pollution generated by Coca-Cola’s Africa branch; logging in Norwegian-owned Green Resources Mozambique, Tanzania, and Uganda; and wildly unethical harvesting of ‘ethical diamonds’ by De Beers, to name a few – accounting firms are allowed to investigate themselves and are absolved from accusations of corruption for this type of behaviour, which falls far outside the neoliberal understanding of corruption.27

Part 2: The Big Heist

Glencore and Zambia

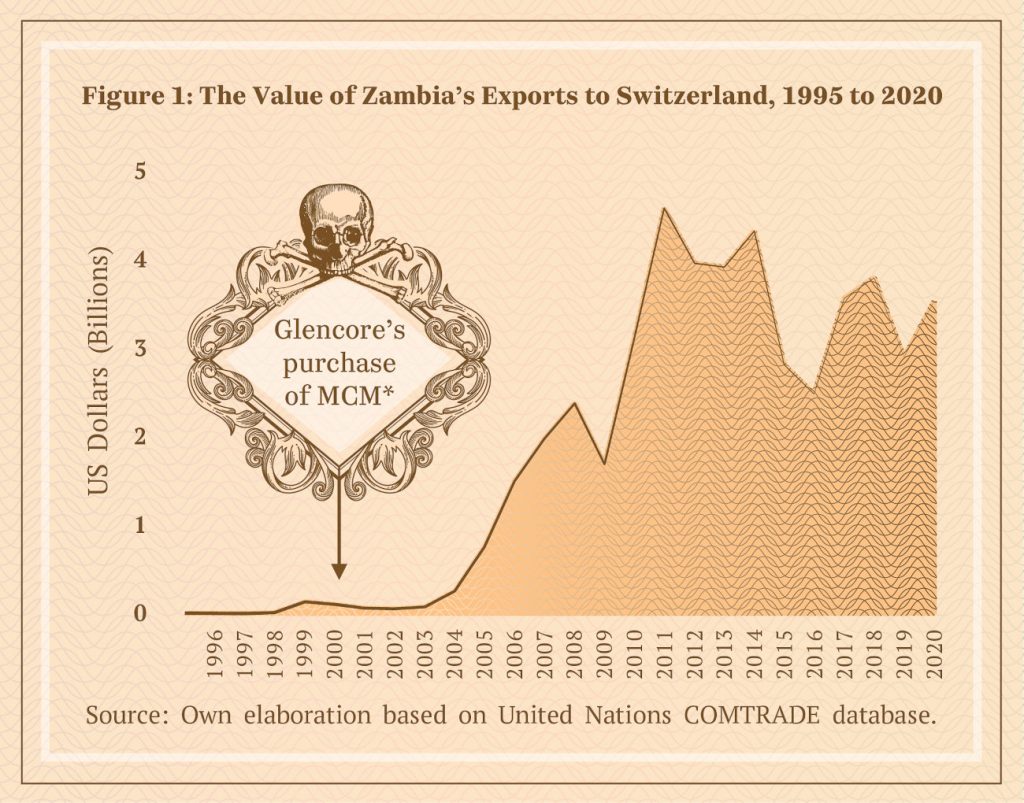

From 2003 to 2023, Zambia’s exports to Switzerland (almost entirely consisting of semi-processed copper) totalled $61 billion – nearly half of the country’s total exports during this period ($145 billion).28 In other words, Switzerland, a tiny landlocked country thousands of kilometres away, has accounted for half of Zambia’s total export market for the last two decades. But it was not always like this.

From 1995 to 1999, for instance, Zambia’s exports to Switzerland, totalling $159 million, made up just 3% of the country’s total exports. This began to change in 2000, when a controlling stake of Mopani Copper Mines (MCM), which up to that point had been owned by the Zambian state, was purchased by Carlisa Investments, a company owned by the giant Swiss commodities trader Glencore AG and domiciled in the British Virgin Islands (itself a tax haven). Therefore, from a legal standpoint, MCM was not owned by Glencore, which allowed Glencore to comply with legal requirements to engage in ‘arm’s length transactions’ with MCM on paper (meaning that they are parties acting independently without influencing each other) while doing the opposite in practice. It is illegal for a company to purchase from and sell to itself (one of the few regulations in place to prevent MNCs from committing tax evasion). However, a company – such as Glencore – can create a subsidiary company – such as Carlisa – with whom it can carry out transactions as if it were a separate company ‘at arm’s length’ while still exercising full influence over the terms and prices in practice. Since it is the subsidiary – Carlisa, in this case – that owns a third company – MCM – Glencore’s transactions with MCM are technically between two independent entities. Efforts are made to ensure that there is no paper trail suggesting otherwise.

* We chose to refer to Glencore as the owner of the mine because in practice, and in common knowledge, Glencore is the owner of the mine. Since Glencore uses Carlisa to obscure its theft of wealth from Zambia, often by shifting its profits around to evade taxes through transfer pricing, we have chosen not to mirror their language of obscurity in this dossier.

As figure 1 shows, Zambia’s annual exports to Switzerland skyrocketed from virtually zero prior to Carlisa’s (i.e., Glencore’s) purchase of MCM in 2000 to nearly $4 billion in 2020. This pattern led many to suspect that Glencore was engaging in transfer pricing – shifting its profits from a high-tax jurisdiction (Zambia) to a low-tax jurisdiction (Switzerland) in order to pay the least possible amount of taxes and maximise its net profits. In other words, instead of having to pay 30% in corporate taxes on the sale of copper in Zambia based on the commodity’s true value, Glencore is able to price the value of copper sales near zero through its relationship with Carlisa and pay taxes on that artificially low amount. Then it pays corporate income taxes in Switzerland at a rate of 14.6% – nearly half the rate it would have had to pay in Zambia.29

In 2010, the Zambia Revenue Authority took Glencore to court for engaging in transfer pricing. Despite arguing that its transactions with MCM were ‘arm’s length’ transactions between two unrelated entities – MCM and Glencore – (after all, MCM was owned by Carlisa, not Glencore), Glencore lost and was instructed to pay a penalty in addition to lost taxes due to transfer pricing.30 After a costly, ten-year legal battle, the decision was upheld by Zambia’s Supreme Court – a landmark ruling that had wider implications for the future taxation of multinational corporations in Zambia and the region. Yet, even so, the penalty levied was a paltry $13 million – a far cry from the hundreds of millions, perhaps billions, of dollars that Glencore has spirited away from Zambia since 2000.31

Thabo Mbeki’s High-Level Panel on Illicit Financial Flows

In 2011, the United Nations Economic Commission for Africa (UNECA) established the High-Level Panel on Illicit Financial Flows, an outcome of a joint conference hosted by the AU and UNECA. In the words of the panel’s chairperson Thabo Mbeki, this was done in the interest of ensuring ‘Africa’s accelerated and sustained development, relying as much as possible on its own resources’ and ensuring ‘respect for the development priorities it had set itself’. After all, Mbeki said, ‘progress on this agenda could not be guaranteed if Africa remained overdependent on resources supplied by development partners’.32

The panel conducted in-depth analytical studies, interviews, and site visits over the course of several years before delivering a 120-page report to the AU in 2015. The report suggested that, even by conservative estimates, Africa was in fact a net lender of capital to the world – not a net borrower, as is the common perception. In other words, if not for theft on this grand scale, Africa would have all the necessary capital within its borders to meet its developmental aspirations.

The very same multinational corporations that had been billed as partners in Africa’s quest for development were making off with most of the continent’s wealth.

The report focused on illicit financial flows out of Africa, which it defined as ‘money illegally earned, transferred, or used’. ‘In other words’, the report continued, ‘these flows of money are in violation of laws in their [country of] origin, or during their movement or use, and are therefore considered illicit’. Some activities, though ‘not strictly illegal in all cases’, the report explained, could be categorised as ‘illicit’ since they ‘go against established rules and norms, including avoiding legal obligations to pay tax’.33

The report estimated that from 2000 to 2010, illicit financial flows out of Africa ranged between $30 billion and $60 billion per year, or a total of between $300 billion and $600 billion over the entire 10-year period. Yet, it was careful to state that the true magnitude of illicit financial flows were likely many orders of magnitude higher than the estimates provided, since, as Chairperson Mbeki wrote, ‘those responsible [for illicit financial flows] take deliberate and systematic steps to hide them’.34 For instance, another report on illicit financial flows, produced by Global Financial Integrity in 2015, found that Africa lost $675 billion in illicit financial flows from 2004 to 2013 while the developing world as a whole lost $7.8 trillion during this period, with these flows increasing twice as fast year-on-year as global Gross Domestic Product.35

Importantly, and perhaps without precedent for an inter-governmental analysis, the Thabo Mbeki Report, as it came to be known, revealed that the majority of illicit financial flows out of Africa (about 65%) were due to legally sanctioned commercial activities whose purpose was ‘hiding wealth, evading or aggressively avoiding tax, [and] dodging customs duties and domestic levies’.36 Multinational corporations’ standard way of limiting tax liabilities, the report explained, was to make false declarations, whether about undervaluing export receipts, overvaluing the costs of business with the ultimate purpose of limiting profits, or, in the extreme case, falsely declaring losses. One intriguing example in the report was that of an unnamed telecommunications giant which was causing the host government to lose an estimated $90 million annually through methods such as ‘diverting international calls and transforming them into local calls, with operators then making fake declarations of incoming international call minutes to reduce the tax payable to the [host] government’.37

Though many governments and multilateral agencies committed to implementing the reports’ recommendations when it was published in 2015, there is little to show for these promises as capital continues its unimpeded flight from Africa.

Part 3: Five Ways to Make Money from Africa

In his 1963 book Africa Must Unite, Ghana’s first President Kwame Nkrumah wrote, ‘We have here, in Africa, everything necessary to become a powerful, modern, industrialised continent. United Nations investigators have recently shown that Africa, far from having inadequate resources, is probably better equipped for industrialisation than almost any other region in the world’. Nkrumah was referring to the United Nations’ Special Study on Economic Conditions and Development, Non-Self-Governing Territories (1958), which detailed the continent’s immense natural resources. ‘The true explanation for the slowness of industrial development in Africa’, Nkrumah wrote, ‘lies in the policies of the colonial period. Practically all our natural resources, not to mention trade, shipping, banking, building, and so on, fell into, and have remained in, the hands of foreigners seeking to enrich alien investors and to hold back local economic initiative’.38

How exactly do alien investors go about making money from ‘everything necessary’ for Africa’s sovereign development? We decided to put together a five-point guide that begins to answer that question.

- Working with the IMF, World Bank, and World Trade Organisation to encourage (i.e., coerce) African governments to implement ‘investor-friendly’ policies. By ‘investor-friendly policies’, we mean the kinds of policies that make it easy to bring capital into Africa and use that capital to extract as much wealth as possible from the continent. Examples of such policies include privatising vital social services (health and education are key); enacting tax incentives that make it possible for investors to pay zero taxes; eliminating labour rights so that workers can be exploited as much as possible; and liberalising the host country’s capital account, which makes it easy to extract all the profits made in Africa.

- Investing in the extractives sector, but not in manufacturing. The trick is to invest in those sectors that make it easy to make a quick buck while hiding behind a veil of opacity. There is no better sector to do this than extractives in Africa, whether drilling oil in Angola, collecting coltan in the Congo, or capturing natural gas in Mozambique. The sites of extraction in this sector are often in enclaves far away from capital cities and, therefore, away from the prying eyes of regulators and the citizenry, thus providing the necessary cover to extract as many resources as possible. Furthermore, investing in extractives rather than manufacturing promises the perpetual underdevelopment of Africa and, therefore, guarantees that the continent will forever be vulnerable to extractive capital – an investment that just keeps giving.

- Engaging in transfer pricing. Transfer pricing is a time-tested technique developed by MNCs to expatriate as much profit as possible from the Global South. The subsidiary company in Africa ‘sells’ its products to the so-called parent company in the West, which subsequently sells the product to the ultimate beneficiary and, therefore, pockets the profits in the West. For example, a Swiss-owned mining operation in the Congo sells its cobalt to its parent company in Switzerland for a price that is nearly zero; the Swiss company then sells the cobalt to the ultimate buyer located at an electric car company in the US at the true value of the cobalt. The general idea with transfer pricing is to pay as little taxes as possible in Africa while booking the profits in the West and paying moderate taxes there.

- Exaggerating production costs. Remember that since corporate taxes are levied on profits, anything that fictitiously reduces profits reported in Africa also limits the taxes that the corporation is obliged to pay. The example of transfer pricing is one way to reduce the profits reported in Africa. Another trick is to exaggerate costs incurred on the continent in ways that the authorities cannot verify. For example, a consulting company, located in the West, can provide expensive ‘consulting services’ to an African operation in a way that limits the profits in Africa and shifts them to the West. Another cost exaggeration gimmick is to grant a non-existent loan to an African subsidiary: interest payments on this fake loan serve to exaggerate production costs in Africa and, therefore, limit profits that must be reported there, instead shifting them to the West.

- Hiring one of the Big Four accounting firms. The Big Four accounting firms – all British – are Deloitte, PricewaterhouseCoopers, Ernst & Young, and Klynveld Peat Marwick Goerdeler. Their stamp of approval is golden, and their audited reports are treated as legal documents. Instead of using information barriers (so called ‘ethical walls’) as they were intended – to ensure the independence and objectivity of the tax advice, consulting services, and auditing – these firms obscure the fact that, often, the same firm provides consulting services while also auditing the hiring company’s books – including auditing these consulting services. For instance, a firm proposes an operational optimisation plan or aggressive tax planning, and that same firm is the ‘independent auditor’ that oversees this plan and then issues an allegedly unbiased opinion that the financial statements are fair. Due to the reduction of state capacity, many African governments now rely upon the reports of accounting firms as uncontested statements of the truth about the operations of MNCs. The hefty fees demanded by the Big Four are very much worth the investment for MNCs, given the hundreds of billions of dollars that they save in taxes.

These five points allow MNCs to make off with Africa’s wealth while ensuring that the continent remains underdeveloped, and yet they are conceptualised as smart business strategies rather than a form of corruption or theft. These actions are legitimised by the hegemonic discourse of corruption, which has taken a decisively neoliberal direction that seeks to dismantle state regulation and protect MNCs. Actual corruption – which manifests both in the corruption of MNCs and the petty corruption of public officials – must be tackled head on, indeed with a clarity that does not exist at present.

Will there ever be an AU Convention on Corporate Corruption?

Notes

1 Transparency International, The Anti-Corruption Plain Language Guide (Berlin: Transparency International, 28 July 2009), 14, https://images.transparencycdn.org/images/2009_TIPlainLanguageGuide_EN.pdf.

2 Daniel W. Barnes et al., Public Office, Private Interests: Accountability Through Income and Asset Disclosure (Washington, DC: World Bank Group, 16 March 2012), ix.

3 ‘Taking the Temperature: Corruption Perceptions Index 2010’, Transparency International (blog), 26 October 2010, https://blog.transparency.org/2010/10/26/cpi2010_temperatures_up/.

4 International Labour Organisation, ‘Country Profiles’, ILOSTAT, accessed 29 September 2024, https://ilostat.ilo.org/data/country-profiles/.

5 Mr Ke-young Chu and Mr Richard Hemming, Public Expenditure Handbook: A Guide to Public Policy Issues in Developing Countries (Washington, DC: International Monetary Fund, 1991).

6 Manenga Ndulo and Edna Kambala, ‘Transfer Mispricing in Africa: Contextual Issues’, Southern African Journal of Policy and Development 4, no. 1 (1 May 2018).

7 For more on this concept, see Tricontinental: Institute for Social Research, The World in Economic Depression: A Marxist Analysis of Crisis, notebook no. 4, 10 October 2023, https://thetricontinental.org/dossier-notebook-4-economic-crisis/.

8 Syed Hussein Alatas, The Problem of Corruption (Kuala Lumpur: The Other Press, 2015), 64. This edition is built on the original 1968 text by Alatas called The Sociology of Corruption.

9 For more, see Tricontinental: Institute for Social Research, Resource Sovereignty: The Agenda for Africa’s Exit from the State of Plunder, dossier no. 16, 7 May 2019, https://thetricontinental.org/wp-content/uploads/2019/05/190503_Dossier-16_EN_Final_Web.pdf and The Congolese Fight for Their Own Wealth, dossier no. 77,25 June 2024, https://thetricontinental.org/dossier-77-the-congolese-fight-for-their-own-wealth/.

10 Ellen Gutterman, ‘The Legitimacy of Transnational NGOs: Lessons from the Experience of Transparency International in Germany and France’, Review of International Studies 40, no. 2 (April 2014): 391–418.

11 Barbara Crutchfield George, Kathleen Lacey, and Jutta Birmele, ‘The 1998 OECD Convention: An Impetus for Worldwide Change in Attitudes Toward Corruption in Business Transactions’, American Business Law Journal 37, no. 3 (2000).

12 Morris Szeftel, ‘Misunderstanding African Politics: Corruption and the Governance Agenda’, Review of African Political Economy 25, no. 76 (June 1998): 221.

13 Parliament of the Republic of South Africa, ‘Finance Committee Outraged by Irregularities in Steinhoff’, Press Release, 6 December 2018, https://www.parliament.gov.za/press-releases/finance-committee-outraged-irregularities-steinhoff.

14 ‘FSCA Levies Record R1.5 Billion Fine against Steinhoff International Holdings N.V. for False, Misleading and Deceptive Statements to the Market’, Herbert Smith Freehills, 20 September 2019, https://www.herbertsmithfreehills.com/notes/fsrandcorpcrime/2019-09/fsca-levies-record-r1-5-billion-fine-against-steinhoff-international-holdings-n-v-for-false-misleading-and-deceptive-statements-to-the-market; ‘Steinhoff Will Only Have to Pay R53 Million of Its R1.5 Billion Fraud Fine’, BusinessTech, 12 September 2019, https://businesstech.co.za/news/business/340685/steinhoff-will-only-have-to-pay-r53-million-of-its-r1-5-billion-fraud-fine/.

15 Robert K. Merton, Social Theory and Social Structure. Toward the Codification of Theory and Research (Glencoe, Illinois: The Free Press, 1949).

16 Edward Shils, ‘Political Development in the New States’, Comparative Studies in Society and History 2, no. 3 (April 1960): 385. Based on fieldwork in a number of African states, a number of scholars developed the argument of Merton and Shils, see M. McMullan, ‘A Theory of Corruption’, The Sociological Review 9, no. 2 (July 1961) and Colin Leys, ‘What Is the Problem with Corruption?’, The Journal of Modern African Studies 3, no. 2 (August 1965): 215–230.

17 Samuel Huntington, Political Order in Changing Societies (New Haven and London: Yale University Press, 1968), 70.

18 For more on the NIEO, see Tricontinental: Institute for Social Research, Sovereignty, Dignity, and Regionalism in the New International Order, dossier no. 62, 14 March 2023, https://thetricontinental.org/dossier-regionalism-new-international-order/.

19 See Vijay Prashad, ed., Selected Ho Chi Minh (New Delhi: LeftWord Books, 2022).

20 For more, see Ernesto ‘Che’ Guevara,‘Socialism and Man in Cuba’, in Ernesto ‘Che’ Guevara: On Socialism and Internationalism (New Delhi: LeftWord Books, 2020), 83, https://thetricontinental.org/text-che/.

21 See United Nations, Commission on Transnational Corporations, Report on the Special Session (7–18 March and 9–21 May 1983), Economic and Social Council Official Records, 1983, supplement no. 7, E/1983/17/Rev. 1 (New York: United Nations, 1983), https://www.google.com/url?sa=t&source=web&rct=j&opi=89978449&url=https://digitallibrary.un.org/record/204950/files/E_1983_17_Rev-1-EN.pdf%3Fln%3Dar&ved=2ahUKEwigz5aL7cSJAxXxqVYBHctSLlcQFnoECBYQAQ&usg=AOvVaw2la6mtRlj4cq6wQh3gbHLy; United Nations Economic and Social Council, Code of Conduct on Transnational Corporations, UN Document, E/RES/1987/57 (10 June 1987), https://digitallibrary.un.org/record/156251?ln=en&v=pdf.

22 United Nations Conference on Trade and Development (UNCTAD), Global Value Chains and Development: Investment and Value Added Trade in the Global Economy (New York: United Nations, 2013), iii, https://unctad.org/system/files/official-document/diae2013d1_en.pdf; United Nations Conference on Trade and Development (UNCTAD), Trade and Development Report 2018: Power, Platforms, and the Free Trade Delusion (New York and Geneva: United Nations, 2018), https://unctad.org/system/files/official-document/tdr2018_en.pdf.

23 ‘Corruption Perceptions Index’, Transparency International, 30 January 2024, https://www.transparency.org/en/cpi/2023.

24 Bill De Maria, ‘Neo-Colonialism Through Measurement: A Critique of the Corruption Perception Index’, Critical Perspectives on International Business 4, no. 2/3 (2 May 2008): 184–202; Faiz-ur-Rahim and Asad Zaman, ‘Corruption: Measuring the Unmeasurable’, Humanomics 25, no. 2 (June 2009): 117–126.

25 United Nations Office on Drugs and Crime, United Nations Convention Against Corruption (New York: United Nations, 2004), https://www.unodc.org/documents/brussels/UN_Convention_Against_Corruption.pdf; African Union, African Union Convention on Preventing and Combating Corruption, adopted 1 July 2003, https://au.int/sites/default/files/treaties/36382-treaty-0028_-_african_union_convention_on_preventing_and_combating_corruption_e.pdf.

26 ‘What Is ESG Investing and Analysis?’, CFA Institute, 4 March 2024, https://www.cfainstitute.org/en/rpc-overview/esg-investing.

27 Adenike Abati, ‘Examining Coca-Cola’s Role in Global Plastic Pollution’, Climate Action Africa, 17 November 2021, https://climateaction.africa/coca-colas-role-in-global-plastic-pollution/; World Rainforest Movement, ‘Green Resources Mozambique: More False Promises!’, WRM Bulletin, no.235 (9 January 2018), https://www.wrm.org.uy/bulletin-articles/green-resources-mozambique-more-false-promises; Matthew Gavin Frank, ‘De Beers: Destruction Is Forever’, EcoWatch, 17 March 2021, https://www.ecowatch.com/de-beers-diamond-mining-greenwashing-2651117844.html.

28 United Nations, ‘UN Comtrade Database’, accessed 5 November 2024, https://comtradeplus.un.org/.

29 PricewaterhouseCoopers, ‘Zambia: Corporate – Taxes on Corporate Income’, PwC World Tax Summaries, accessed 5 November 2024, https://taxsummaries.pwc.com/zambia/corporate/taxes-on-corporate-income; PricewaterhouseCoopers, ‘Switzerland: Overview’, PwC World Tax Summaries, accessed 5 November 2024, https://taxsummaries.pwc.com/switzerland.

30 ‘Zambia Court Ruling Against Copper Mining Company Is a Victory Against Abusive Tax Practices’, African Tax Administration Forum, 1 June 2020, https://www.ataftax.org/zambia-court-ruling-against-copper-mining-company-is-a-victory-against-abusive-tax-practices.

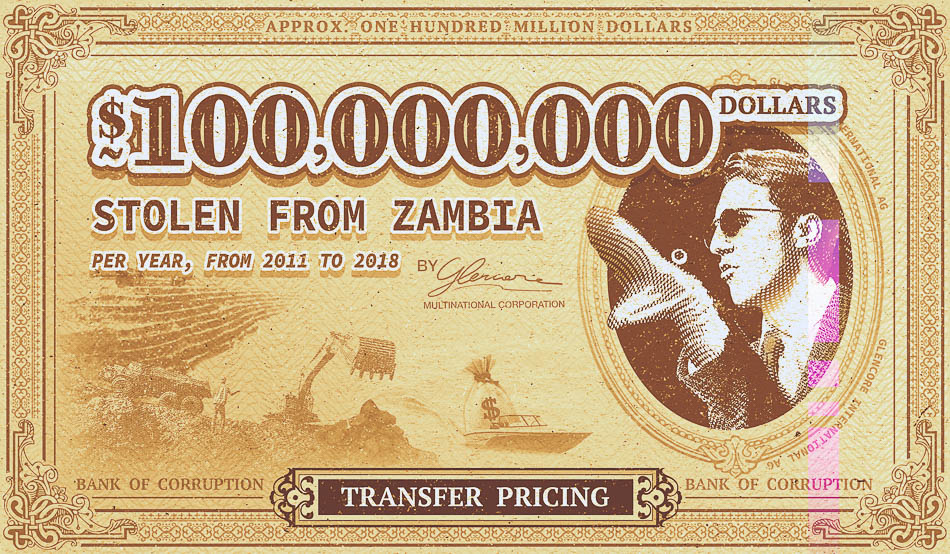

31 A 2021 Oxfam study estimated that Glencore was underpaying its taxes in Zambia by about $100 million per annum between 2011–2018. See Daniel Mulé and Mukupa Nsenduluka, ‘Potential Corporate Tax Avoidance in Zambia’s Mining Sector? Estimating Tax Revenue Gains from Addressing Profit Shifting or Revising Profit Allocation Rules. A Case Study of Glencore Mopani Copper Mines’, Oxfam Research Backgrounder series, 9 December 2021, https://www.oxfamamerica.org/explore/research-publications/potential-corporate-tax-avoidance-in-zambias-mining-sector/.

32 High Level Panel on Illicit Financial Flows from Africa, Illicit Financial Flows: Report of the High Level Panel on Illicit Financial Flows from Africa (Addis Ababa: United Nations Economic Commission for Africa, 2015), 2, https://au.int/en/documents/20210708/report-high-level-panel-illicit-financial-flows-africa.

33 High Level Panel, Illicit Financial Flows, 15.

34 High Level Panel, Illicit Financial Flows, 3.

35 Dev Kar and Joseph Spanjers, Illicit Financial Flows from Developing Countries: 2004–2013 (Washington, DC: Global Financial Integrity, December 2015), https://34n8bd.p3cdn1.secureserver.net/wp-content/uploads/2015/12/IFF-Update_2015-Final-1.pdf.

36 High Level Panel, Illicit Financial Flows, 24.

37 High Level Panel, Illicit Financial Flows, 28.

38 Kwame Nkrumah, Africa Must Unite (New York: Frederick A. Praeger, 1963), 23–24, https://ccaf.africa/books/Africa-Must-Unite-Kwame-Nkrumah.pdf.

Sources referenced in the artworks

- Accounting fraud: ‘Government nails Steinhoff for R6.2 billion’, BusinessTech.

- Transfer pricing: Daniel Mulé and Mukupa Nsenduluka, ‘Potential Corporate Tax Avoidance in Zambia’s Mining Sector? A Case Study of Glencore Mopani Copper Mines’, Oxfam Research Backgrounder series.

- Sustainability reporting: World Rainforest Movement, ‘Green Resources Mozambique: More False Promises!’, WRM Bulletin, no. 235.

- Illicit financial flows: Dev Kar and Joseph Spanjers, Illicit Financial Flows from Developing Countries: 2004–2013, Global Financial Integrity.