The Architecture of Power: The Dollar, Financialisation, and the Struggle for Sovereignty

The role of the dollar as the principal currency of exchange in world trade grants the United States exorbitant power. This dossier examines the rise of this currency, the mechanisms of its domination, and the structural limits to building an alternative to the dollar.

In a capitalist society, money performs an essential function. It is the material representation of an immaterial social relation: value, which is established through the labour of millions of people across the world. Money serves as a means of exchange, a unit of account, and a way of storing that value. Yet money is never neutral. When a specific national currency transcends its borders to become a world currency, it becomes a powerful instrument of hegemony, discipline, and imperial power.

The history of the last two hundred years is the history of the rise and contestation of two such key currencies: the British pound sterling in the nineteenth century, and, far more expansively, the US dollar from the twentieth century to the present.

The current global order, underpinned by the dollar, grants the United States what has appropriately been called an ‘exorbitant privilege’: the power to issue the currency that the rest of the world needs as a store of value, means of payment, and unit of account.1 This allows the United States to finance its deficits, consume more than it produces, and project its military power simply because its public debt is treated as the safest asset on the planet. It also enables the United States to host the world’s most important financial market, shaping expectations that extend far beyond the financial sphere and influencing investment and production worldwide. In turn, these financial flows establish key conditions that determine the direction of global finance and limit the autonomy of dependent and subordinated countries.

National currencies exist within a hierarchy defined in relation to the dollar. For countries of the Global South, this architecture imposes a high cost. Their currencies are treated as volatile financial assets, and their economies are held hostage to the discipline imposed by international financial capital. The need to accumulate dollars as a defence against speculative attacks and to guarantee imports results in a perverse net transfer of wealth from the Global South to the Global North, particularly to investors and speculators in Western Europe and the United States. Given these structural features of contemporary capitalism, understanding the rise of the dollar, the mechanisms of its present domination, and the structural limits facing any alternative is therefore a central task for those who seek a more just and cooperative international order.

Money, Value, and the Need for a World Currency

In any society based on the division of labour and the exchange of commodities, money emerges as a practical necessity. When different producers specialise – one growing wheat, another making cloth, yet another extracting ore – they need to exchange their products with each other in order to meet their needs. But direct exchange, or barter, presents obvious difficulties: the farmer who wants cloth must find a weaver who at that same moment wants wheat, in the exact amount, and accepts the proposed exchange ratio.

Money solves this problem by functioning as a universal equivalent: a special commodity that everyone accepts in exchange for any other. With money, the farmer can sell wheat to any buyer, keep the value received, and later buy cloth from any seller. Money thus fulfils three basic functions: it serves as a means of circulation, facilitating exchange; a unit of account, allowing the value of different commodities to be compared; and a store of value, allowing wealth to be preserved for future use.

In Marxist analysis, money is not an arbitrary invention or a mere technical instrument. It is the material expression of a social relation called value. The value of a commodity corresponds to the socially necessary labour time required to produce it. When millions of independent producers exchange commodities on the market, they are, in practice, comparing quantities of human labour. Money is therefore the form through which that comparison becomes possible and visible. It represents social labour in condensed form.2

Within a single country, the use of money is relatively simple: there is a national currency, issued and guaranteed by the state, which all inhabitants recognise and accept. But what happens when producers in different countries want to trade with one another? Let us consider a concrete example. A Brazilian company exports coffee to Germany. The German importer has euros, while the Brazilian exporter needs reais to pay workers, suppliers, and taxes. How can these two currencies be reconciled? The problem unfolds on several levels. First, an exchange rate must be established: how many reais are equivalent to one euro? Second, there must be a mechanism to convert one currency into the other. Third, both parties must trust that the currency they receive will hold its value and be accepted by others.

When international trade was small-scale and sporadic, such problems could be resolved on a case-by-case basis, often with universally accepted precious metals such as gold and silver. But as the world market expanded, that solution became insufficient. As international trade grew, there emerged a need for an organised system to settle accounts between countries. It is not practical for each individual transaction to involve either the physical transfer of gold or the direct conversion of one currency into another. A clearing mechanism is needed. Imagine that, over a given period, Brazil exports US$100 million in coffee to Germany and imports US$80 million in machinery. Rather than making two separate transfers, the two amounts are offset against each other, and Germany only needs to transfer the net difference of US$20 million to Brazil. This is the principle of clearing.

For such a mechanism to work on a global scale, involving dozens of countries and currencies, a common reference point is required – a currency that everyone accepts as a unit of account and means of payment for settling balances. Historically, that role was first played by gold and later by the national currencies of economically dominant countries. The advantages associated with controlling the reference currency are anything but simple. They include:

- the possibility for the issuing state to expand its capacity for debt and spending disproportionately in relation to other national states;

- the use of the currency as an instrument of foreign policy and domination through control over key channels of international liquidity, as in the case of economic sanctions; and

- the advantages granted to the international operations of its banks, which, because they operate within a fractional reserve system backed by a currency that can be expanded, occupy a privileged position in the circuit of global high finance.

This gives rise to fundamental questions: who issues this reference currency? Through what mechanisms does it become dominant? What are the consequences when a country’s national currency is elevated to the status of a world currency?

The World Market Expands and Imperial Currencies Take Hold

Since the sixteenth century, the expansion of the world market has been driven by colonial conquest, the trafficking of enslaved people, the seizure of land and natural resources, and the imposition of unequal trading relations on subjugated populations. Originary accumulation, which Marx analysed in the first volume of Capital, was a global and violent process.3 As capitalism consolidated itself as the dominant mode of production, the volume of international trade grew exponentially.

In the eighteenth century, the Industrial Revolution intensified this process: the European powers needed raw materials from across the world, such as cotton, minerals, and agricultural products, and sought markets for their manufactured goods. This growth made the problem of an international currency increasingly urgent. With thousands of daily transactions between dozens of countries, an organised international monetary system became indispensable: a set of rules, institutions, and practices that defined how currencies relate to one another, how payments are settled, and how trade imbalances are adjusted. The solution adopted in the nineteenth and early twentieth centuries reflected the power structure at the time: a world divided among competing colonial empires. Each imperial power organised its own monetary zone, integrating its colonies and spheres of influence into a system of trade, credit, taxation, and payments centred on its national currency.

As the leading industrial, commercial, and financial power of the nineteenth century, Britain made the pound sterling the principal currency of international trade, enforcing its system of ‘imperial preferences’ on the rest of the world. The so-called gold standard, which prevailed from the 1870s until 1914, was in practice a sterling-gold standard: sterling was the currency in which most trade contracts were denominated, major commodities were priced, and international loans were issued.

The sterling system’s dominance as an international currency was made possible by draining wealth from the colonies. India maintained large current-account surpluses (meaning that it earned more from exports and other external payments than it spent abroad) with continental Europe, the United States, Canada, and Japan, but it ran a current-account deficit with Britain (meaning that it paid more to Britain than it received from it). This was partly because of British exports to India and, above all, the obligations imposed by the British on the colony, including ‘gifts’ of huge sums of wealth transferred from British India to the metropole.4 As S. B. Saul writes in Studies in British Overseas Trade 1870–1914, ‘The key to Britain’s whole payments pattern lay in India, financing as she probably did more than two-fifths of Britain’s total deficits’.5

The British colonies – from India to Africa and the Caribbean to Oceania – were integrated into the metropole’s monetary zone through the British system of imperial preferences. Their exports were quoted in sterling; their imports, largely supplied by Britain because of the metropole’s trade monopoly, were paid for in sterling; and their banking systems operated with sterling as their reference currency. Colonial populations were forced to obtain sterling to pay taxes and buy essential goods, which subordinated them entirely to the terms of trade set by the metropole.

The French colonial empire – stretching across North and West Africa, Indochina, and islands in the Pacific and the Caribbean – constituted its own monetary zone based on the franc. To this day, remnants of that structure survive in the CFA franc, used by fourteen African countries and tied first to the French franc, then to the euro.6 Although they did not possess a formal colonial empire comparable to those of the European powers, the United States exercised economic hegemony over much of the Americas from the late nineteenth century onwards. An early expression of this ambition was the Monroe Doctrine (1823), often summarised by the phrase ‘America for the Americans’, which opposed further European colonisation or intervention in the Americas while asserting the United States’ claim to regional pre-eminence. The dollar circulated widely in Central America, the Caribbean, and parts of South America, often imposed through military interventions and the presence of US companies that controlled strategic sectors, such as the United Fruit Company in Central America. Germany, Japan, the Netherlands, Belgium, and Portugal also maintained their own colonial monetary spheres, although on a smaller scale.

The result was a fractured international monetary system. There was no world currency but rather several competing regional currencies, each dominant within its own sphere of influence. Though sterling was the most important globally, it was not universal. This system reflected the structure of imperialism as analysed by Lenin and other Marxists in the early twentieth century: a world divided among rival capitalist powers, each controlling its own bloc of colonial and semi-colonial territories. The tensions between these blocs – the struggle for markets, raw materials, and fields of investment – were among the primary causes of the First World War (1914–1918).7

The war destroyed this order. It demanded colossal expenditures, financed through monetary issuance and indebtedness. Most countries suspended gold convertibility. Britain, once the world’s great creditor, emerged as a debtor. The United States, which entered the war late and supplied the Allies, became the primary international creditor.

The interwar period (1918–1939) was marked by failed attempts to restore the gold standard, chronic exchange-rate instability, competitive devaluations – the so-called currency wars – and the collapse of international trade following the crisis of 1929. The Great Depression showed that a disorganised international monetary system was incompatible with the ‘stability’ of capitalism.

The Second World War (1939–1945) created the conditions for a radical reorganisation. The United States emerged from the conflict as the only major power whose economy was not only intact but strengthened. Though global power was now shared with the Soviet Union, the United States stood out as the leading capitalist power: it was willing to keep capital flows relatively open, allow foreign claims on US assets, and use its currency as a world currency. By the end of the war, the United States held around two-thirds of the world’s gold reserves and its industry accounted for nearly half of global manufactured output – not to mention that its territory had not been devastated by the war.8 This asymmetry of power allowed the United States to impose a new international monetary architecture. At the Bretton Woods Conference in 1944, a system was created that, for the first time in history, established a single national currency as the axis of the world monetary system: the US dollar.

The Bretton Woods system marked the transition from a world of competing monetary zones linked to rival empires to a single, dollar-centred monetary order led by the United States. This process represented the shift from an inter-imperialist system, characterised by rivalry between multiple powers, to an imperialist model of unipolar order led by the United States in which one dominant power organised the system as a whole.9 This transition was neither automatic nor purely economic. It was the result of war, the destruction of rival powers, the military occupation of former empires such as Germany and Japan, and the construction of a vast network of military bases, alliances, and international institutions under US leadership.

How the Dollar Became Hegemonic

The real consolidation of the dollar as the dominant currency was the result of a strategic project meticulously carried out by the United States during and immediately after the Second World War. The rise of the dollar was not a historical accident; it was the result of three decisive strategic moves.

I. Financing the Wars

The United States used its position as an ‘arsenal of democracy’, a term coined by US president Franklin D. Roosevelt, to structure global dependence on its currency. Initially, the Cash-and-Carry rule of 1937 required buyers of US supplies to pay immediately in dollars or gold and transport the goods themselves, a condition that favoured countries with access to hard currency, gold reserves, and naval capacity.

Later, the Lend-Lease mechanism allowed the United States to supply allied countries with military equipment, food, fuel, and other goods on credit or deferred payment rather than requiring immediate purchase. But it also had a deeper structural effect: by the end of the war, the Allied powers and dozens of other countries had accumulated massive debts denominated in dollars. Given their wartime vulnerability, dependence on US supplies, and limited bargaining power, the United States could impose the currency in which its credits would be denominated. This created a permanent structural demand for the US dollar. Countries now had to export real goods or contract new debts to obtain the dollars required to settle their debt obligations.10

II. Control over Oil

The second pillar was to secure control over the energy source that would fuel postwar industrial capitalism. Oil transformed the logic of conflict from the First World War onwards. It became the central natural resource of the international system, and control over producing regions became a core element of global geopolitical disputes. More specifically, oil became the main fuel of the armed forces and assumed a decisive position in the world transport matrix, and its derivatives, such as fuel, plastics, fertilisers, synthetic materials, and petrochemicals, came to be widely used across countless production chains. This had further implications for international relations: oil became a recurring instrument on the diplomatic chessboard, functioning as a mechanism of pressure, retaliation, deterrence, support, or strategic backing. In other words, states could use access to oil, oil prices, and control over producing regions to reward allies, punish adversaries, and shape geopolitical outcomes.

By 1940 the United States was the dominant oil power, accounting for 63% of global oil production.11 As it became clear that the future centre of gravity of oil production would shift to the Middle East, the United States acted decisively. As early as 1933, US companies had acquired exploration rights in Saudi Arabia. In 1943, President Roosevelt incorporated the Kingdom of Saudi Arabia into the ‘dollar monetary territory’, authorising the financing of Ibn Saud’s kingdom through Lend-Lease. The United States’ intense diplomatic and military activity in the region, which consolidated its dominance over Saudi Arabia, laid the basis for oil from this new nerve centre to be priced and traded in dollars, a process that was institutionalised in the 1970s through the petrodollar system. Saudi Arabia was thus transformed into a US zone of influence and economic space and incorporated into the dollar’s monetary sphere.12 This decision compelled most countries, especially industrialised and energy-importing nations, to join the dollar’s monetary territory. In order to buy energy, they first had to obtain dollars.

In this sense, the imposition of a monetary architecture on the global oil market was more decisive than direct control over production. From the 1970s onwards, this move was institutionalised through the ‘petrodollar’, especially with the oil shocks (the sharp increases in oil prices that followed the 1973 Yom Kippur War and the oil embargo by Arab members of the Organisation of the Petroleum Exporting Countries, or OPEC). Oil-producing Arab states used oil as a political weapon and OPEC price increases helped quadruple the price of oil, pushing the world economy into a severe crisis. In this context, the Nixon administration negotiated a secret agreement with Saudi Arabia. The terms were: the Saudis would sell oil exclusively in dollars and invest their surpluses in US Treasury securities (US government debt instruments such as Treasury bonds). In return, the United States would guarantee military protection to the Saudi kingdom. The other OPEC countries soon followed the same model. By tying the world’s main commodity to its currency, the United States structurally expanded the international reach of the dollar.

III. The Bretton Woods System

In 1944, at Bretton Woods, the United States formalised and institutionalised its hegemony, especially in the economic sphere. In 1945, the Yalta Conference helped reorganise the geopolitical and military order after the war by setting the terms for the occupation of Germany, the division of spheres of influence in Europe, and the postwar balance between the major powers. In monetary terms, the Yalta agreements stipulated that German war reparations would be accounted for in dollars.

At Bretton Woods, two opposing visions of the postwar order collided. The British proposal, led by John Maynard Keynes, was radically different from the one that prevailed. Keynes proposed the ‘Bancor’, a supranational international unit of account that would be controlled by a multilateral body called the Clearing Union. His aim was to create a symmetrical system that would penalise both chronically deficit countries and chronically surplus countries. In essence, Keynes’s proposal sought to prevent the kind of ‘exorbitant privilege’ later associated with the dollar from passing from sterling to the dollar by ensuring that no single national currency could become the anchor of the international monetary system.

Keynes’s proposal was summarily defeated. Given the balance of forces, the US plan, led by Harry Dexter White, prevailed. White’s plan was centred on US power: the dollar would be defined as the international unit of account and would be the only currency with full convertibility into gold, at the fixed rate of US$35 per ounce of gold. All other currencies would maintain convertibility into the dollar at fixed but adjustable exchange rates.

To manage this new order, the International Monetary Fund (IMF) and the International Bank for Reconstruction and Development (IBRD, today the World Bank) were created. The capital of both institutions was defined in dollars, and their structure was designed to guarantee US control. The voting power of each member country was linked to its quota or capital subscription. In the IMF, these subscriptions were paid partly in gold and partly in national currency. In the IBRD, part of the capital had to be paid in gold or dollars. Since the United States held the largest share in both institutions, with Britain in second place, an asymmetrical decision-making structure was consolidated. In the case of the IMF, because crucial decisions require a qualified majority of 85% of the vote, the United States acquired, in practice, veto power over fundamental reforms.13

The Centrality and Decline of Dollar Hegemony in the Twentieth Century

The Bretton Woods system, sometimes called the dollar-gold standard, consolidated the centrality of the dollar and of the United States in the world economy. But the system could not function by itself. It needed liquidity – enough dollars circulating internationally to allow trade, payments, and reconstruction to take place. The devastated economies of Europe and Japan did not have the dollars needed to import inputs, restart exports, or rebuild cities, infrastructure, and productive apparatuses.

The United States solved this problem through the Marshall Plan for Europe (1948–1952) and the Dodge Plan for Japan (1949), which provided the dollars needed to finance reconstruction. These plans ‘saved’ the Bretton Woods system by ensuring that rebuilding Washington’s strategic allies would integrate them fully into the dollar’s monetary territory from the start. At the same time, the United States encouraged the global expansion of its multinational corporations, which entered these reconstructed markets through dollar-denominated direct investment. Because the dollars supplied were, to a great extent, used to buy goods and services produced in the United States itself, the plans also won domestic support from various economic sectors. In a conjuncture of cooling domestic activity, aggravated by the growth of industrial capacity during the war years in Europe and the Pacific, this external demand helped sustain the US economy.

From a strategic standpoint, the United States not only made possible so-called reconstruction and growth ‘miracles’ in several countries, stabilising regions central to the logic of the Cold War, but also consolidated the hegemonic position of the dollar. In the decades that followed, the areas under its influence experienced a long cycle of expansion and prosperity anchored in the centrality of the dollar.

More concretely, while financing economic recovery in regions central to the containment of the USSR, the United States reinforced the primacy of the dollar by:

- injecting dollars directly into allied economies through programmes such as the Marshall Plan;

- significantly expanding its military spending abroad, denominated in dollars, as in the case of the Korean War;

- unilaterally opening its market to exports from strategic partners, thereby guaranteeing them dollar revenues;

- accepting that these countries would maintain artificially undervalued exchange rates, using the dollar as their monetary reference; and

- encouraging outward direct investment from its large corporations, which naturally took place in dollars given the origin of those firms.

In addition, the United States tolerated unilateral controls on cross-border capital movements, accepted the non-convertibility of other currencies, did not react forcefully to protectionist policies, and even sent technical assistance missions. This tolerance was conditional: Washington permitted its allies to use state intervention and trade protections while keeping them within the dollar-centred order.

The Triffin Dilemma

Despite its apparent solidity, the Bretton Woods system contained a fatal contradiction identified by the economist Robert Triffin. The ‘Triffin Dilemma’ exposed the logical flaw in using a national currency as an international one. The contradiction was as follows: for world trade and economic growth to expand, the world needed a growing supply of international liquidity – that is, more dollars. But in order to provide those dollars to the rest of the world, the United States had to run balance-of-payments deficits, meaning that it had to send more dollars abroad through spending, lending, investment, and imports than it received back from abroad. However, by issuing more and more dollars than it held in gold reserves, the United States would inevitably undermine global confidence in the dollar’s convertibility into gold.14 The system was therefore doomed. If the United States stopped running these deficits – that is, stopped supplying the world with dollars – world trade would stagnate. If it continued, confidence in the dollar would collapse.

During the 1960s, this contradiction became critical. Massive increases in US public spending, driven simultaneously by the Vietnam War and domestic social programmes, led to growing deficits and uncontrolled money issuance. At the same time, US hegemony was being challenged by revolutions in the periphery and by criticism from European allies, especially the French. Even the IMF created Special Drawing Rights (SDRs) in 1969 – a synthetic supranational reserve asset nicknamed ‘paper gold’, whose value was based on a basket of currencies – in an attempt to create a source of liquidity that did not depend on US deficits.

In 1971, the Triffin Dilemma reached a breaking point. With surplus countries, led by France, exchanging dollars for gold, US reserves fell drastically. On 15 August 1971, President Richard Nixon acted. In a unilateral decision that reconfigured a system that had been created multilaterally, Nixon suspended the dollar’s convertibility into gold indefinitely. The dollar-gold standard was dead. The world entered a new era: that of flexible exchange rates, financialisation, and a fiat dollar. The hegemonic currency no longer had any backing in a physical commodity; its value was determined purely by confidence – or, more precisely, by the economic, financial, military, and geopolitical power of the United States.

After 1973, in the face of successive devaluations and instability in the dollar’s value, major capitalist countries adopted a regime of ‘floating exchange rates’. In other words, currencies ceased to have fixed parity with the dollar and their value came to be determined in each national economy’s foreign exchange market, where currencies are bought and sold according to demand, supply, interest rates, trade flows, and expectations about each economy.

The Interest-Rate Shock and Dollar ‘Diplomacy’

Faced with growing challenges to the US economy, especially in the economic and monetary spheres, the United States resorted to what came to be known as the interest-rate coup. In response to domestic inflationary pressures and concern over the weakening dollar, Paul Volcker, then chair of the US central bank, the Federal Reserve, raised short-term US interest rates from around 10–11% in 1979 to nearly 20% by late 1980 and early 1981. This sharply increased borrowing costs across the world because much international credit was denominated in dollars or tied to US financial conditions.15

According to the Brazilian economist Maria da Conceição Tavares in her seminal text ‘A retomada da hegemonia norte-americana’ (The Resumption of North American Hegemony), before the interest-rate coup the private banking system had been operating largely beyond the control of central banks, especially the Federal Reserve.16 Transnational branch networks structured a regional division of labour within the firms themselves, often at odds with the national interests of the United States, and fostered growing competition among capitals that proved unfavourable to the US economy. Overall, a world economy without a clearly defined hegemonic pole contributed to the disorganisation of the postwar order and to the growing fragmentation of private and regional interests. From 1979 onwards, with the interest-rate coup, the conduct of US domestic and foreign economic policy moved precisely in the direction of reversing these tendencies and recovering command over international finance.

Tavares used the expression ‘the diplomacy of the strong dollar’ to refer to this unilateral US action, which made deliberate use of US monetary and financial power as an instrument of foreign policy and as a means of reconstructing US hegemony.17 The rise in interest rates cannot be understood only as a monetary policy measure aimed at dealing with domestic US macroeconomic problems. It was a central move in reasserting dollar hegemony and completely restructuring the international monetary and financial system.

When US interest rates are high, wealthy investors leave their positions in other countries and seek gains from the interest-rate differential offered by US public debt – that is, from the higher returns paid by US Treasury securities compared with assets elsewhere. As a result, the Eurodollar market, which had been developing in Europe outside the control of the US central bank, largely returned to the financial centre of Wall Street. That move reinforced US domination over financial capital and strengthened the power of its banking system. In this sense, the US currency was used as a geo-economic weapon: by controlling interest rates, liquidity, and access to international credit through the dollar-centred financial system, the United States disciplined allies, brought competitors into line, and deepened the dependence of the periphery. Thus, the policy of high interest rates and a strong dollar is not merely economics: it is a strategy of power.

This action, however, had consequences. First, it plunged the United States and the rest of the world into a prolonged recession as higher borrowing costs squeezed firms, households, banks, and indebted states. The result was a wave of bankruptcies, including among firms and even some US banks. Second, it caused a sudden contraction of international credit, inflicting damage especially on the capitalist periphery, which had taken advantage of the period of high international liquidity to accumulate dollar debts at floating interest rates – debts whose costs rose sharply once US rates increased. Third, the interest-rate coup led to the recentralisation of interbank credit and the large international banks in New York under the Federal Reserve’s umbrella, placing the international private banking system more firmly under US monetary command.

Another objective of the interest-rate coup was to bring US competitors in line. By the late 1970s and early 1980s, Japan had achieved strong industrial and technological dynamism, generating growing trade surpluses with the United States and appearing to be on a path to becoming the world’s largest creditor as the United States became (and remains) the world’s largest debtor. With high interest rates, the dollar remained overvalued and the enormous returns on US Treasury securities produced a capital inflow into the United States, including from Japan, with Japanese firms and banks buying US Treasury bonds. Even while running trade surpluses, Japan found itself in a position in which it financed the US deficit by buying dollar assets, and its own development became increasingly tied to the US financial system and asset cycle.

When the US trade deficit with Japan exploded and domestic political pressure increased, the second part of the disciplining process began. In 1985, the Reagan administration threatened heavy protectionist measures and forced a coordination agreement in the G5 in what became known as the Plaza Accord. The goal was to bring about a coordinated devaluation of the dollar against the yen and the German mark. The result came quickly: between September 1985 and April 1986, the yen appreciated by around 35% against the dollar, making Japanese exports more expensive, weakening Japan’s trade advantage, and helping contain the yen’s potential as a rival reserve currency.18 Then came the Louvre Accord of 1987, which sought to stabilise exchange-rate parities after this sharp correction. According to Brazilian economists Tavares and Luis Eduardo Melin, this was not a neutral technical adjustment but a political move aimed at consolidating US power: the United States used its position at the centre of the system to force Japan to accept a strong appreciation of the yen and a reorganisation of its growth pattern.19

The United States thus compelled Japan to adjust its growth path, exchange rate, and financial policy to suit the interests of US hegemony. This ensured that the yen would not become a rival reserve currency and that Japanese surpluses would be recycled in ways that benefited the financing of the US deficit and US financial leadership. Rather than a rupture, what occurred was Japan’s reabsorption into an order commanded by the dollar: the country retained high productive sophistication but under strong financial and geopolitical constraints defined in Washington.

How the Dollar Sustains Itself

The collapse of Bretton Woods, paradoxically, did not weaken the dollar. On the contrary, it freed the United States from any material constraint on its monetary policy and consolidated a new form of hegemony, no longer anchored in gold but in three new pillars: oil and petrodollar recycling; the depth and liquidity of US financial markets, especially the market for Treasury securities; and the weaponisation of dollar-based finance.

To understand the post-1971 order, it is crucial to turn to the Marxist analysis of financialisation. The abandonment of metallic backing (gold) was a watershed moment. It removed the material restriction on the limitless creation of money, which had previously been a representation of a commodity (gold) but became a representation of itself – mere numbers in computerised accounts. In other words, there was an autonomisation of the world currency. This allowed capital to migrate massively from the sphere of value production (investment in manufacturing, agriculture, and so on, based on the application of social labour) to the sphere of circulation – that of fictitious capital. Fictitious capital is investment in property titles (shares) and, above all, debt titles (mortgages and public debt), whose value is based not on value already produced but on the anticipation of future income. With the unlimited creation of fiat money (money issued by the state that is not convertible into a commodity such as gold), fictitious capital could feed itself, generating more fictitious capital that was no longer tied to the value base of social labour.

Pillar 1: Oil and Petrodollar Recycling

Though this process began in the 1930s and 1940s, as noted above, after 1971 it took on new importance as the United States reinforced its strategic and military alliance with Saudi Arabia and ensured that OPEC would continue to price and trade oil exclusively in dollars. This recreated structural demand: because every industrialised nation needs oil, every industrialised nation needs dollars. It also created a new recycling mechanism. Oil-producing countries in OPEC accumulated enormous dollar surpluses (petrodollars) from oil sales. These were deposited in Wall Street banks and reinvested in US government debt and other dollar assets, helping to finance US deficits.

Pillar 2: The Dictatorship of Liquidity (Treasuries)

Today, dollar dominance rests on a pragmatic fact: the dollar provides access to financial markets deep enough to absorb very large transactions without sharp price movements and liquid enough to allow assets to be bought and sold quickly. The central pillar of this system is US Treasury securities, which are universally regarded as global ‘safe-haven’ assets: high-grade financial assets with minimal credit risk and immediate liquidity. This allows the United States to completely subvert normal economic logic: it is the world’s largest debtor, yet its debt is treated by other countries as the most valuable asset.

In moments of global financial crisis – even crises that originate in the United States itself, as in 2008 – international capital does not flee the dollar; it rushes towards it, seeking the safety of Treasuries. This flight to Treasuries reinforces the Global Surplus Recycling Mechanism (GSRM), an expanded form of petrodollar recycling in which export surpluses – not only oil revenues – are recycled into US financial assets. It operates as follows:

- The United States absorbs the world’s surplus products, running massive trade deficits with countries such as China, Germany, and Japan.

- The profits from those exports accumulated by the surplus countries (in dollars) return to Wall Street because those countries recycle the dollars they receive from exports into US public debt.

- Wall Street uses this inflow of foreign capital to buy Treasuries, financing the deficit of the US government and supplying credit to US consumers so that they can continue consuming imported goods.

Under this system, the rest of the world is forced to finance the twin deficits of the United States – trade and fiscal – thereby subsidising US consumption and, crucially, its global military power.

In Latin America, this process accelerated after the recommendations of the Washington Consensus, which urged countries to give up controls over their capital accounts (the channels through which investment, loans, and other cross-border financial flows enter and leave a country). This means that capital can enter and leave each country freely, but it has direct effects on the volatility of national exchange rates. Countries, in turn, seek to protect themselves from this volatility by accumulating foreign reserves in US public debt. That is why we can say that the dollar is a weapon of extortion against the periphery: to protect their domestic economies from exchange-rate volatility and capital flight, countries in the periphery must accumulate dollar reserves, often in US public debt. In doing so, they help finance the United States’ twin deficits (trade and fiscal), which in turn sustain US military spending, overseas bases, imperialist wars, and so on.

The crisis of 2008 was the moment when the ‘pyramids of private money’ (fictitious capital) built by Wall Street on top of this mechanism collapsed. Yet the crisis did not break the system. Instead, the Federal Reserve acted as the central bank of the world, supplying dollar swap lines (agreements that allowed other central banks to obtain dollars from the Federal Reserve and provide them to their own financial systems in moments of stress). This proved that, in the collapse, dependence on the dollar was total rather than showing that the dollar had become dispensable.

Pillar 3: Currency as a Weapon of War

Because most global trade, finance, and commodity transactions – especially oil – are denominated in dollars and cleared through the US financial system, Washington has gained enormous coercive power. Dollar ‘diplomacy’ is used both to constrain strategic enemies and to reward allies. The United States can impose financial sanctions, freeze the reserves of foreign central banks – as it has done with Iran, Venezuela, and Russia, for instance – and exclude entire countries from the international payments system (SWIFT).

When a country is sanctioned, as happened to Cuba, Iran, Venezuela, Afghanistan, Russia, and many others, it can be excluded from dollar payment networks and may have its foreign assets frozen. This raises the cost of imports; blocks access to credit and payment systems; obstructs the purchase of food, fuel, medicine, and industrial inputs; and makes ordinary trade far more difficult. The dollar, therefore, is not merely an economic tool: it is a weapon of war, an instrument of geopolitical discipline that ensures US interests prevail.

Is De-dollarisation Already Underway?

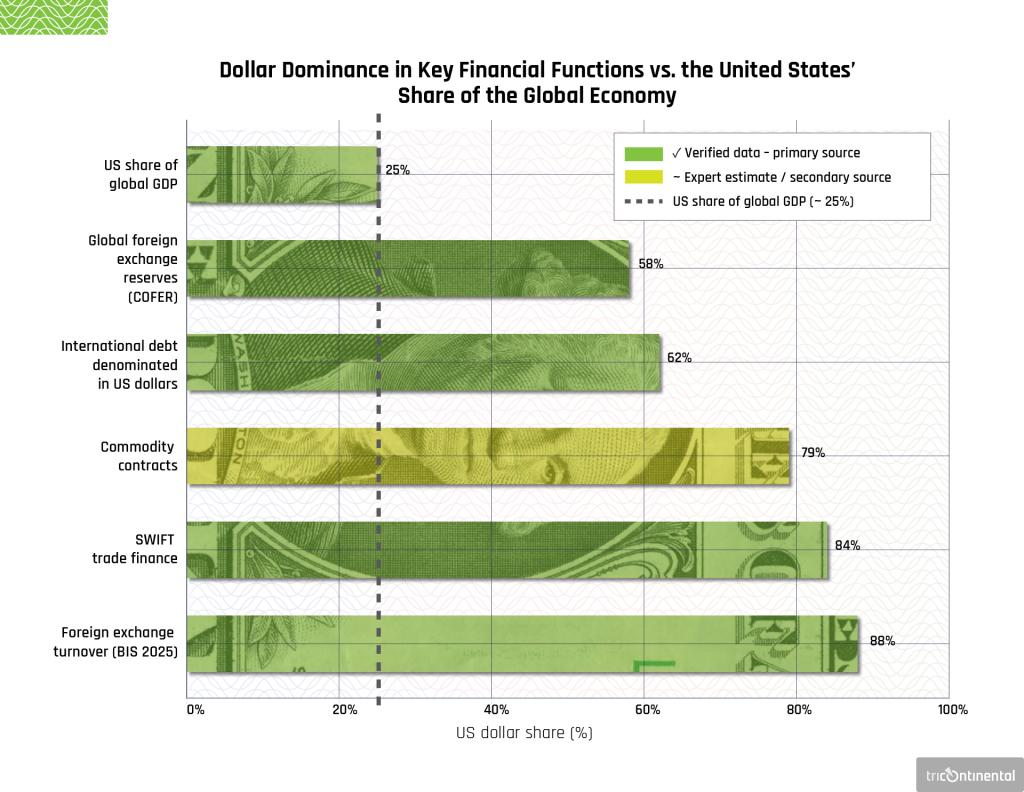

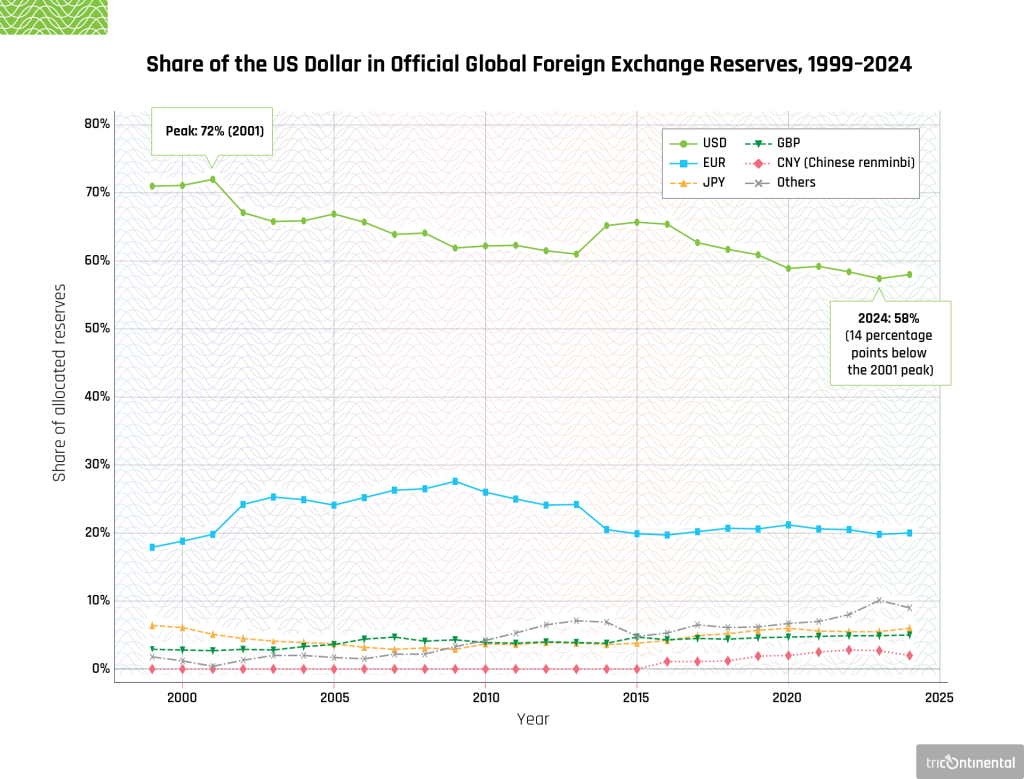

Data on the currencies used in trade invoicing and international finance is scarce, and it is published with longer delays than other trade data.20 Even so, the available evidence indicates that the dollar’s predominance exceeds the weight of the United States’ share of global gross domestic product, trade, and international finance, reflecting a structural asymmetry in the international use of currencies.

Sources: BIS Triennial Survey 2025 · SWIFT Watch 2024 · IMF COFER 2024 · Federal Reserve 2025

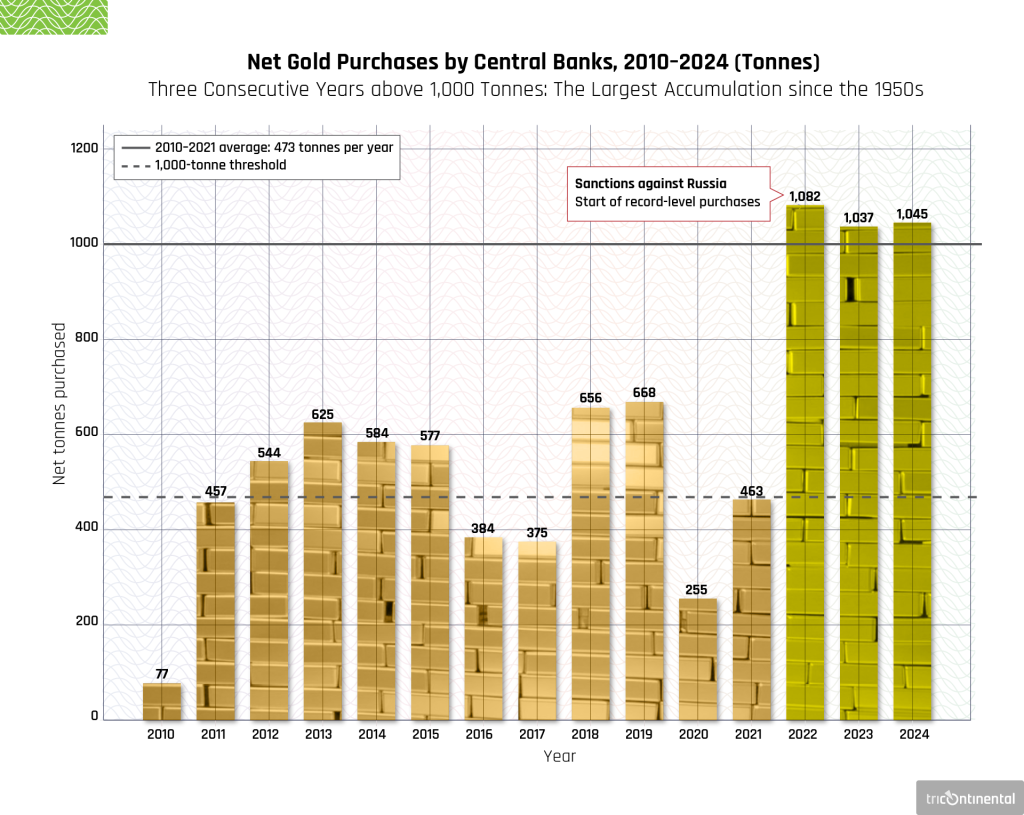

SWIFT data shows that the dollar is used in more than 80% of trade-finance transactions processed through its network, largely because a significant share of commodity trade continues to be invoiced and settled in dollars. In addition, the dollar still accounts for close to 60% of global foreign exchange reserves. On the other hand, the evolution of global foreign exchange reserves in 2022–2023 was marked by a significant increase in gold purchases by central banks. Considered a safe asset, gold offers protection against geopolitical risks, even though it has limitations as a means of payment. This pattern suggests that the intensification of gold purchases by certain central banks is associated with efforts to mitigate economic and geopolitical risks, especially those related to international sanctions. In China, for example, the share of gold in total reserves rose from less than 2% in 2015 to 4.3% in 2023, while the proportion of assets denominated in US Treasury and agency securities fell from around 44% to approximately 30%, reflecting a recomposition of the country’s reserve portfolio.21

Source: World Gold Council, Gold Demand Trends: Full Year 2024 (gold.org)

Although a decline in the dollar’s share of global foreign exchange reserves has been observed in recent decades, the data indicates that this movement does not correspond to a direct substitution by another single currency. On the contrary, the reduction has been absorbed by a set of currencies that the IMF classifies as ‘non-traditional currencies’: the Australian dollar, Canadian dollar, South Korean won, Swedish krona, and, to a lesser extent, the Chinese renminbi. Taken together with the increase in gold reserves, this suggests that the process currently underway is not driven primarily by a coordinated political project of de-dollarisation but rather by portfolio diversification strategies adopted by monetary authorities oriented towards risk management and greater security in a context of growing global financial instability.

This movement can be interpreted as a response to the contradictions of US- and Europe-driven financialisation, whose dynamics tend to generate recurring volatility and asset bubbles (sharp rises in prices that often end in collapse). In this sense, reserve diversification (the spreading of foreign-exchange reserves across a wider range of currencies and assets) appears less as a political rupture than as a technical adjustment to the system’s fragilities. This makes the process of transforming the international monetary system both more robust and slower than more immediate geopolitical narratives suggest.

Source: IMF COFER | Federal Reserve, The International Role of the US Dollar, 2025 edition | The CNY series excludes data for the fourth quarter of 2016

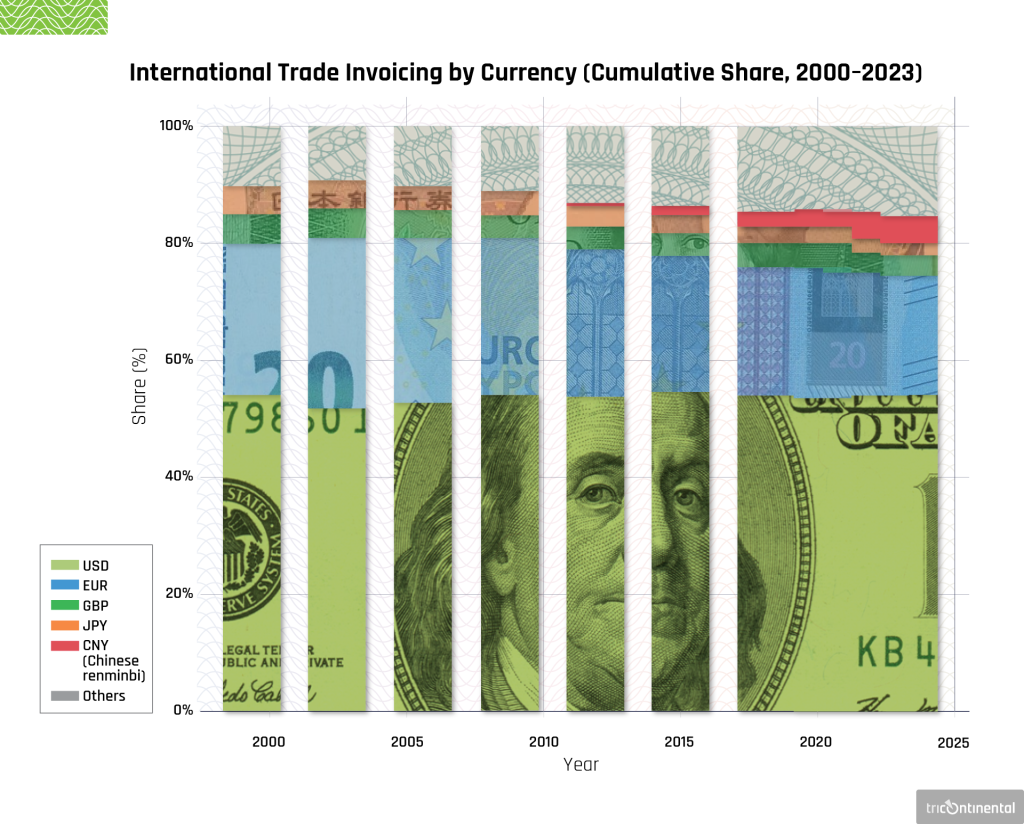

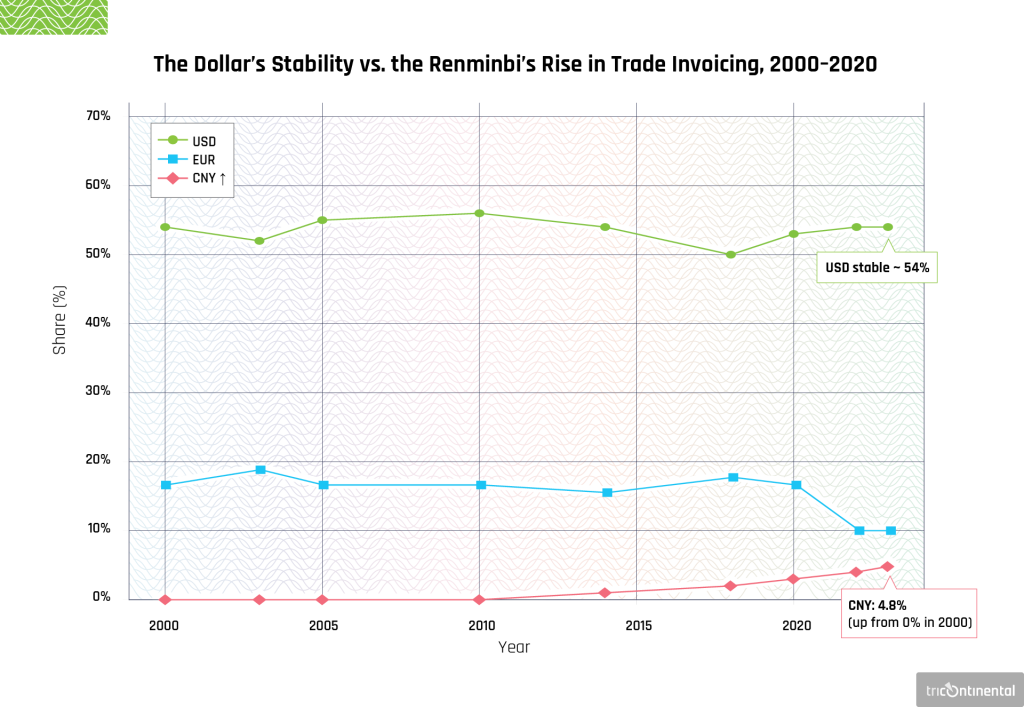

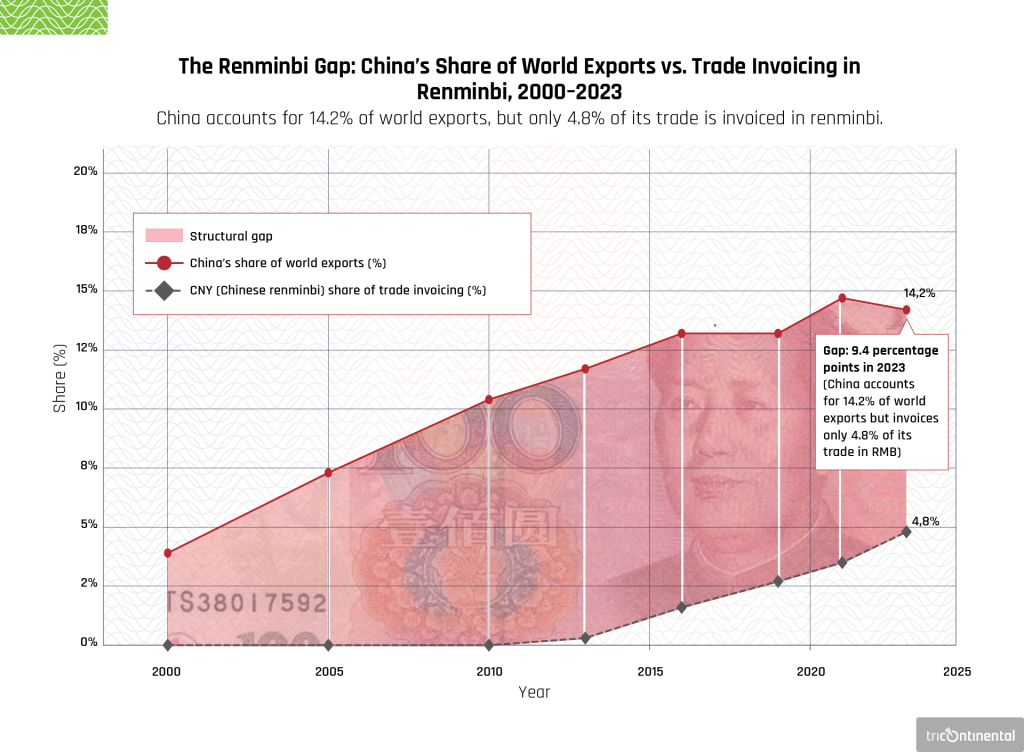

An analysis of trade invoicing from 2000 to 2023 shows that the combined share of the dollar and the euro remained broadly stable. The dollar retained its dominant position, while the euro was used predominantly within the European Union. Although China has significantly expanded its share of world exports since 2000, approaching that of the United States, the renminbi remains limited as a currency for international trade invoicing and has not been fully internationalised.

These data demonstrate the resilience of the dollar in trade invoicing. They also show that, although the renminbi’s share of international reserves has grown notably, broader monetary diversification remains limited.

Source: IMF Working Paper (2025), Patterns of Invoicing Currency in Global Trade in a Fragmenting World Economy

Source: IMF Working Paper (2025), Patterns of Invoicing Currency in Global Trade in a Fragmenting World Economy

Source: IMF Working Paper (2025), Patterns of Invoicing Currency in Global Trade; IMF Direction of Trade Statistics (DOTS) Patterns of Invoicing Currency in Global Trade

Advances in financial technology and payment infrastructure are driving the rise of alternative systems of payment, asset custody, and settlement. These are becoming concrete alternatives to the dollar-centred international financial system. Far from being a recent debate, this is the materialisation of new institutional architectures capable of enabling transactions outside of the traditional circuits. Noteworthy initiatives include the Financial Messaging System (SPFS, developed by Russia) and the Cross-Border Interbank Payment System (CIPS, led by China), which expand the capacity for international settlement in local currencies and reduce dependence on infrastructures dominated by the core countries.

At the same time, the BRICS countries have intensified efforts to strengthen domestic digital payment systems and develop solutions for cross-border operations with the aim of expanding international trade denominated in local currencies and advancing the construction of a more multipolar monetary system.22 China, in particular, has expanded the international use of the renminbi by developing CIPS and participating in central bank digital currency (CBDC) projects.23 There has also been a rapid global spread of CBDC projects: 137 countries and monetary unions, representing around 98% of world GDP, are at some stage of developing these digital currencies.24

At the same time, initiatives such as mBridge (involving the People’s Bank of China, the Hong Kong Monetary Authority, the Central Bank of the United Arab Emirates, and the Bank of Thailand, with the support of the Bank for International Settlements) and the ACUMER system (developed by the Central Bank of Iran) signal the potential of new digital infrastructures for settlement in local currencies between central banks through CBDCs without the need for traditional intermediaries such as correspondent banks or systems like SWIFT.

Moreover, bilateral currency swap agreements have played a growing role, especially since the financial crisis of 2007–2008. These instruments have been used to provide liquidity in moments of stress and to reduce the costs associated with the accumulation of international reserves. This enables countries to access foreign currencies without relying exclusively on international financial markets. In this sense, currency swaps have become a central component of contemporary strategies for monetary diversification and for mitigating dependence on the dollar.25

In sum, the available data indicates that while the dollar remains dominant and relatively stable in the international monetary system, there are also important changes in the composition and functioning of that system. One significant example is the renminbi, whose share of international reserves rose from virtually zero at the start of the 2010s to around 2.2% in less than a decade – a historically unprecedented development for the currency of a country that still maintains important controls over its capital account. This growth in reserve holdings has not, however, been matched by a comparable expansion of the renminbi’s use in international trade invoicing.

An analysis of de-dollarisation therefore requires a distinction between different dimensions of the international monetary system. In the sphere of foreign exchange reserves, the process is slow and gradual and still far from amounting to a rupture with the centrality of the dollar. In the sphere of bilateral payments there is more dynamism, though still geographically concentrated in specific arrangements, such as transactions between Russia and China, which, according to a report published in November 2025, are settled 99.1% in roubles and yuan.26 Finally, in the field of financial infrastructure, which includes payment, clearing, and settlement systems, the process is still incipient but has a structural character, given that the creation of these platforms tends to reduce dependence on the dollar-centred financial system in a lasting way.

In this sense, the importance of de-dollarisation lies in the direction in which this transformation moves and, above all, in the construction of institutional and productive alternatives capable of reducing the costs of exiting the dollar system.

To De-dollarise Is to Fight for Sovereignty

For the overwhelming majority of countries in the Global South, the international monetary and financial system centred on the dollar is not a safety net but a straitjacket. Insofar as countries need to accumulate international reserves – hard currencies such as the dollar – they are subjected to monetary extortion by the dollar system, since they must maintain those reserves and do so by purchasing US public debt. In doing so, they continue to finance the outsized capacity of the United States to act, including by funding wars. Furthermore, the system is also a mechanism of punishment, since the United States can, through sanctions, blockades, and exclusion from the international payments system, penalise countries that are not subservient to it. In recent decades, Washington has increased economic sanctions against the targets of its foreign policy by 933%.27

In practice, national currencies are not seen as stores of value but as volatile ‘financial assets’. International demand for them is speculative, subject to panic and capital flight. In addition, Global South countries suffer from the structural inability to issue external debt in their own currencies. They borrow in dollars but generate revenue in local currency, creating a devastating currency mismatch: when their currencies depreciate, they must use more local currency to obtain the same amount of dollars needed to service their external debts.

Dollar hegemony is therefore not limited to the dollar’s centrality as a means of payment or store of value. It also expresses itself in the way the dollar’s domestic dynamics are transmitted to the rest of the world. In moments of dollar appreciation, peripheral currencies tend to depreciate, making imports more expensive and putting pressure on domestic inflation, especially in economies that are dependent on energy, food, and intermediate goods. Because a large share of international commodities is priced in dollars, these effects are amplified even in the absence of variations in the real conditions of supply and demand.

In financial markets, decisions in US monetary policy, such as interest-rate hikes, frequently trigger capital flows towards dollar-denominated assets. This causes exchange-rate depreciations, raises the cost of external financing, and restricts the space for economic policy in countries of the Global South, which are often forced to adopt contractionary measures to contain inflation and stabilise their currencies – even in contexts of low growth. In economies with high levels of debt in foreign currency, dollar appreciation immediately raises the burden of that debt in domestic-currency terms, deepening structural fragilities. In order to attract volatile international capital, assets in the Global South must offer much higher interest rates than the ‘safe’ assets of the North. This results in a constant net transfer of wealth from poorer countries to the richest financial centres.

With neoliberal policies and the liberalisation of capital movements, the capacity of states to conduct macroeconomic policy has been weakened. Any government that attempts to implement expansionary fiscal or monetary policies, such as cutting interest rates to stimulate investment, is immediately punished by the ‘market’ through capital flight, which devalues the currency, generates inflation, and can lead to collapse. Governments become hostages to the confidence of financiers. To protect themselves from this volatility, Global South countries are forced to accumulate massive international reserves. Brazil, for instance, held more than US$358 billion in December 2025.28 These reserves are mostly invested in dollar assets, especially US Treasury securities. This is the final paradox: to defend themselves from the system, Global South countries are obliged to finance their oppressor, lending trillions of dollars to the US Treasury at low interest rates.

Dollar hegemony imposes unsustainable costs on the Global South. Dissatisfaction with this destabilising asymmetry is not new, but it has taken on renewed urgency in a world moving towards multipolarity. De-dollarisation has become a long-term structural trend, though one that faces immense structural obstacles. According to the economist Bruno de Conti, several developments may, in the medium or long term, trigger changes in the international monetary and financial system, namely:

- the redefinition of the role of certain countries in the hierarchy of the world economy;

- the intensification of geopolitical tensions among the leading powers; and

- the growing distrust of the dollar, sharpened during the Trump administration, combined with the political willingness of a broad set of countries to seek ways to reduce their dependence on the US currency, whether individually or in coordination.29

The discussion of de-dollarisation, however, cannot be reduced to protection against sanctions or the mitigation of external vulnerabilities. A deeper analysis must ask what purpose de-dollarisation is meant to serve. The replacement of one hegemonic currency by another does not necessarily imply a qualitative transformation of the international order, nor does it guarantee greater stability or benefits for peripheral countries. Historical experience suggests that monetary hierarchy tends to reproduce itself, albeit in new configurations.

De-dollarisation must be understood not merely as a dispute between currencies but as part of a broader debate about the nature of international economic relations. For countries of the Global South, this means shifting the focus away from the mere substitution of instruments and towards the construction of structural alternatives involving new forms of participation in international trade, technological cooperation, productive integration, and political coordination. An effective transformation of the international monetary system would therefore require more than the creation of alternative financial mechanisms. It would require confronting the pillars that sustain dollar hegemony, including the centrality of commodity pricing, the dominance of dollar-denominated financial markets, and the capacity for geopolitical coercion.

De-dollarisation is not an end in itself but part of a broader struggle for economic sovereignty and for the construction of a more equitable international order capable of interrupting the systematic transfer of wealth from the Global South to the centres of power. The struggle for de-dollarisation, therefore, is not merely an accounting adjustment. It is a fundamental political struggle over sovereignty, development, and the right of the peoples of the Global South to organise their economies outside the discipline of imperial finance.

Notes

1 Batista Jr., ‘The BRICS and the Challenge of De-Dollarisation’.

2 Marx, Capital, vol. 1.

3 Marx, Capital, 1.

4 Patnaik and Patnaik, A Theory of Imperialism.

5 Saul, Studies in British Overseas Trade, 1870–1914, 58, 88, quoted in Patnaik and Patnaik, A Theory of Imperialism, 126.

6 Metri, História e diplomacia monetária.

7 Lenin, Imperialism.

8 Mazzucchelli, Os dias de sol.

9 Tricontinental, Hyper-Imperialism.

10 Metri, História e diplomacia monetária.

11 Quintas, ‘Os EUA e a geopolítica imperialista do petróleo’.

12 Metri, ‘A ascensão do dólar e a resistência da libra’.

13 Batista Jr., O Brasil não cabe no quintal de ninguém.

14 Akyüz, ‘Política de resposta à crise financeira global’.

15 Tavares, ‘A retomada da hegemonia norte-americana’, 157–67.

16 Tavares, ‘A retomada da hegemonia norte-americana’, 160.

17 Tavares, ‘A retomada da hegemonia norte-americana’.

18 Melin, ‘O enquadramento do iene’.

19 Tavares and Melin, ‘A reafirmação da hegemonia norte-americana’.

20 Gopinath, ‘Geopolitics and Its Impact on Global Trade and the Dollar’.

21 Gopinath, ‘Geopolitics and Its Impact on Global Trade and the Dollar’.

22 Atlantic Council, ‘Dollar Dominance Monitor’.

23 It is important to distinguish central bank digital currencies (CBDCs) from private cryptocurrencies. CBDCs are a form of money in the strict sense: they are issued and guaranteed by national monetary authorities and perform the classical functions of money. Private cryptocurrencies, such as Bitcoin, have no state backing; they are speculative assets without a productive basis, whose circulation and valuation remain subordinate to the dollar-based monetary order.

24 Atlantic Council, ‘Central Bank Digital Currency Tracker’.

25 Council on Foreign Relations, ‘Central Bank Currency Swaps Tracker’.

26 Politics Today, ‘Russia and China Settle 99% of Trade in National Currencies’.

27 Metri, História e diplomacia monetária.

28 Banco Central do Brasil, ‘Série Temporal 13621’.

29 Conti, ‘As iniciativas dos BRICS’.

Bibliography

Atlantic Council. ‘Dollar Dominance Monitor’. 2024, https://www.atlanticcouncil.org/programs/geoeconomics-center/dollar-dominance-monitor/.

Atlantic Council. ‘Central Bank Digital Currency Tracker’. 2024, https://www.atlanticcouncil.org/cbdctracker/.

Akyüz, Yılmaz. ‘Política de resposta à crise financeira global: questões fundamentais para os países em desenvolvimento’ [Policy Response to the Global Financial Crisis: Key Issues for Developing Countries]. Revista Tempo do Mundo 2, no. 3, December 2010: 147–85.

Banco Central do Brasil (BCB). ‘Série Temporal 13621: Investimento direto – passivo – ingresso líquido (US$ milhões)’ [Time Series 13621: Direct Investment – Liabilities – Net Inflow (US$ Millions)]. 2026, https://www3.bcb.gov.br/sgspub/consultarvalores/consultarValoresSeries.do?method=consultarSeries&series=13621.

Batista Jr., Paulo Nogueira. O Brasil não cabe no quintal de ninguém: bastidores da vida de um economista brasileiro no FMI e nos BRICS e outros textos sobre nacionalismo e nosso complexo de vira-lata [Brazil Does Not Fit in Anyone’s Backyard: Behind the Scenes of a Brazilian Economist’s Life at the IMF and the BRICS and Other Texts on Nationalism and Our Inferiority Complex]. LeYa, 2019.

Batista Jr., Paulo Nogueira. ‘The BRICS and the Challenge of De-Dollarisation’. Tricontinental: Institute for Social Research, 17 May 2024, https://thetricontinental.org/wenhua-zongheng-2024-1-brics-dedollarisation-opportunities-challenges/.

Conti, Bruno de. ‘As iniciativas dos BRICS para a transformação do sistema monetário e financeiro internacional’ [BRICS Initiatives for the Transformation of the International Monetary and Financial System]. Nota no. 15. Projeto Transforma Economia – Unicamp, 2025, https://transformaeconomia.org/as-iniciativas-dos-brics-para-a-transformacao-do-sistema-monetario-e-financeiro-internacional/.

Council on Foreign Relations (CFR). ‘Central Bank Currency Swaps Tracker’. 2025, accessed 19 March 2026, https://www.cfr.org/trackers/central-bank-currency-swaps-tracker.

Gopinath, Gita. ‘Geopolitics and Its Impact on Global Trade and the Dollar’. International Monetary Fund, 8 May 2024, https://www.imf.org/en/news/articles/2024/05/07/sp-geopolitics-impact-global-trade-and-dollar-gita-gopinath.

International Monetary Fund (IMF). ‘2025 External Sector Report: Global Imbalances in a Shifting World’. July 2025, https://imf.org/-/media/files/publications/esr/2025/english/text.pdf.

International Monetary Fund (IMF). ‘Patterns of Invoicing Currency in Global Trade in a Fragmenting World Economy’. IMF Working Paper, 2025, https://www.imf.org/en/publications/wp/issues/2025/09/12/patterns-of-invoicing-currency-in-global-trade-in-a-fragmenting-world-economy-570297.

Lenin, Vladimir. Imperialism, the Highest Stage of Capitalism. International Publishers, 1939.

Marx, Karl. Capital: A Critique of Political Economy, Volume 1. Translated by Ben Fowkes. Penguin, 1976.

Mazzucchelli, Frederico. Os dias de sol: a trajetória do capitalismo no pós-guerra [Days of Sun: The Trajectory of Capitalism in the Post-war Period]. Facamp, 2013.

Melin, Luis Eduardo. ‘O enquadramento do iene: a trajetória do câmbio japonês desde 1971’ [The Framing of the Yen: The Trajectory of Japanese Exchange Rates since 1971]. In Poder e dinheiro [Power and Money], edited by José Luís Fiori. Vozes, 1997.

Metri, Maurício. ‘A ascensão do dólar e a resistência da libra: uma disputa político-diplomática’ [The Rise of the Dollar and the Resistance of the Pound: A Political-Diplomatic Dispute]. Revista Tempo do Mundo 1, no. 1, January 2015.

Metri, Maurício. História e diplomacia monetária [History and Monetary Diplomacy]. Dialética, 2023.

Patnaik, Utsa and Prabhat Patnaik. A Theory of Imperialism. New York: Columbia University Press, 2016.

Politics Today. ‘Russia and China Settle 99% of Trade in National Currencies’. 6 November 2025, https://politicstoday.org/russia-and-china-settle-99-of-trade-in-national-currencies/.

Quintas, Felipe Maruf. ‘Os EUA e a geopolítica imperialista do petróleo’ [The US and the Imperialist Geopolitics of Oil]. Associação dos Engenheiros da Petrobras (AEPET), n.d., https://aepet.org.br/artigo/os-eua-e-a-geopolitica-imperialista-do-petroleo/.

Saul, S. B. Studies in British Overseas Trade 1870–1914. Liverpool: Liverpool University Press, 1960.

Tavares, Maria da Conceição. ‘A retomada da hegemonia norte-americana’ [The Resumption of North American Hegemony]. Revista de Economia Política 5, no. 2 (18), April–June 1985: 157–67.

Tavares, Maria da Conceição and Luis Eduardo Melin. ‘A reafirmação da hegemonia norte-americana’ [The Reaffirmation of North American Hegemony]. In Poder e dinheiro [Power and Money], edited by José Luís Fiori. Vozes, 1997.

Tricontinental: Institute for Social Research. Hyper-Imperialism: A Dangerous Decadent New Stage. Studies on Contemporary Dilemmas no. 4, 23 January 2024. Compiled by Global South Insights (GSI), edited by Gisela Cernadas, Mikaela Nhondo Erskog, Tica Moreno, and Deborah Veneziale. https://thetricontinental.org/studies-on-contemporary-dilemmas-4-hyper-imperialism/.